u/Roadtochessmaster

r/IMadeThis r/TikTok r/lichess r/Polymarket r/Stocks_Picks r/Anduril r/Achievements r/YouTubeEditorsForHire r/Substack r/PredictionsMarkets r/sui r/biotech r/Investing101 r/VideoEditors r/Anthropic

▲ 3 r/Achievements

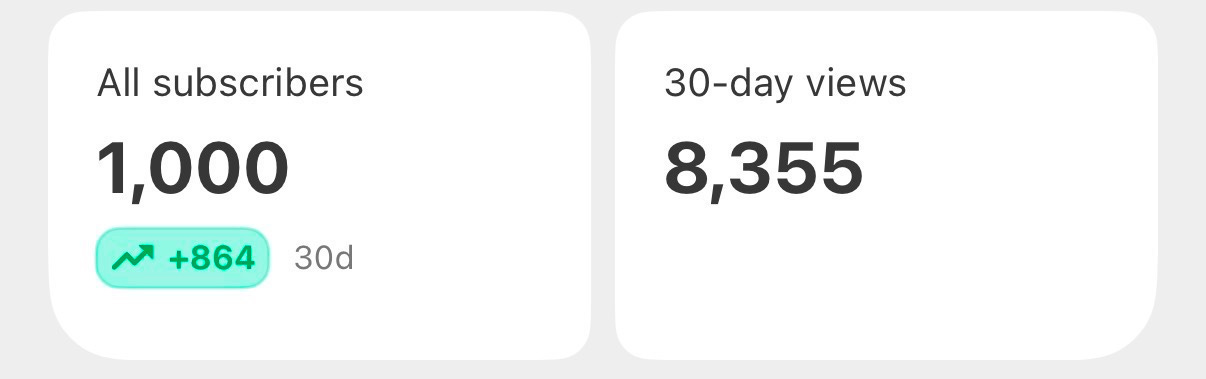

Reached 1400 on Substack!

Been 10 weeks on the platform and loving it!!

Started with 0 and through hard work and commitment I am here in around 70 days.

{kind=link}

u/Roadtochessmaster — 1 day ago

▲ 12 r/Substack

What I learned from growing from 0-1000 in 40 days.

My first account had about 30 subscribers in a month. When I began my second, it was with all the tips I learned from my failures in my first account.

I realize I got partly lucky with my growth, but here are my 5 tips that helped me grow to 1000 subscribers in 40 days without any external help.

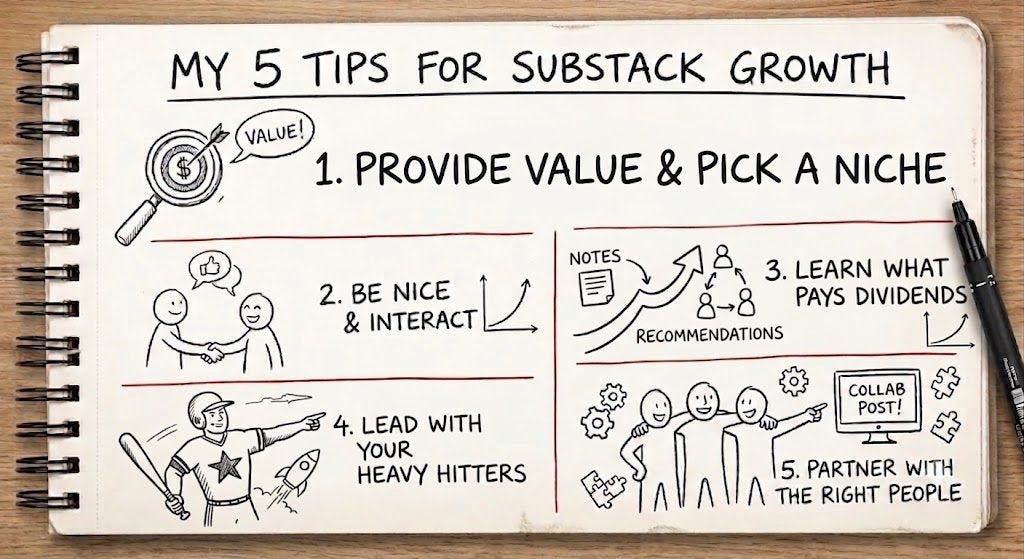

#1 Provide Value and Pick a Niche.

This one is pretty simple, people will only subscribe if your content is providing value, people will be more likely to subscribe if that content is unique to your page.

#2 Be Nice and Interact.

Scroll while liking, comment meaningful things when you read posts you enjoy, connect with other writers and build connections. Those connections pay dividends down the line.

#3 Learn What Pays Dividends.

Focus on notes and recommendations for growth, articles for sustained retention.

#4 Lead With Your Heavy Hitters

Post your best content today, don't wait - there might be news that shifts the focus of attention elsewhere while you hold your best post for when you "get bigger".

#5 Partner With The Right People.

Partner with the people who will increase the value of your post, not just those who have the biggest audiences.

Hope this helps!

u/Roadtochessmaster — 1 day ago

▲ 0 r/Substack

How I grew to 1000+ Subscribers in 40 days.

Just wrote this post on Substack about growth. I write about finance in general but was getting dozens of questions about what I did to grow on Substack.

Figured I would just write it in an article instead, genuine tips that helped me, hope it helps you all as well!

--------------------------------------------------------------------------------------------

This is a different post than those I am used to putting out. Dozens of people have asked me questions about growth advice on Substack or about advice in beginning a Substack. For those people, this is for you. For my regular subscribers who aren’t interested in building their own Substack, I still think you will find interest in this post. In any case, next week’s post will be a regular breakdown of a private company.

Reaching 1000 subscribers is a milestone that I thought would take me months, at best if not years. Instead, within forty days of starting this account, I hit 1000 subscribers.

{kind=link}

It’s a huge milestone and one that I don’t take for granted. After all, this isn’t my first Substack account. I began writing in February and after almost three months, I had reached almost 200 subscribers, a feat I thought was rather impressive.

So when I began this account, it was with minimal help, a few (no more than a couple dozen) dedicated subscribers who moved over when I mentioned that I will be starting a new account. Aside from those twenty or so people, 98% of the growth that I had in getting to 1000 subscribers was entirely organic and replicable.

And for those looking to replicate it, these are the relatively simple tips that I have that might help you. This isn’t anything revolutionary, but it’s tips that I would have appreciated knowing when I began writing on Substack and therefore tips that I feel would be worth sharing.

A note of honesty: I could be wrong about some of these tips, they are just what I found to have helped me grow.

Tip One: Provide Value and Pick a Niche.

This one goes without saying but people will continue to read your work only if it provides value to them. That doesn’t mean that it needs to be focused on growing your stock portfolio or providing financial value.

Some people enjoy learning just for the sake of learning and any interesting content will be up their alley. Others, are looking for advice on different personal topics. A number of other people require emotional support.

In any case, providing value in a certain niche is the most important growth requirement for any Substack account. Ideally, you want the value to be tangible and the niche to be specific and unique.

For me, my value proposition is simple.

I take a complex and murky area of finance (private companies) and break those companies down so that the average person who wants to learn about them can.

The value proposition is tangible. These are companies that can be invested in either now or in the future. The niche is specific, I only focus on companies that are currently private. The content is unique as not many people are covering private companies.

If you want to grow your Substack account, find a unique niche and provide value.

Tip Two: Be Nice and Interact.

Unless you get extremely lucky, every writer will eventually experience the same feeling. The feeling that you invested hours into an article that got minimal traction… I definitely did.

There’s no other way to put it; it sucks to write an article that you spent a dozen or more hours on to get 4 likes and 0 comments.

And yet, all it takes to reverse this is one comment from a reader. One person who thought that your article was worth reading and commenting for that feeling to disappear - or at least be alleviated in a major way.

I myself have had this feeling a number of times, on my post on Isomorphic Labs, despite putting an enormous amount of work into the article which included interviewing a PhD researcher who I highly recommend (The Pharma Fox) only one person commented on the post. This one person was truly the difference between feeling that no one read my post and a bunch of people read my post. I’d like to publicly thank Soul Hacked AI Labs for that comment.

As a writer, you likely know this feeling and you probably know it well. Why not try to help alleviate others of the feeling that they are writing to a brick wall?

{kind=link}

How it feels writing a post and getting 0 comments.

>

For the altruistic among us, supporting other creators makes others happy, and you should want to do this for the sake of making the world a better happier place.

For the spiritual people here supporting other writers creates good karma that will likely eventually find its way back to you.

For those who have finite time and are focused on furthering their platform, I truly believe that supporting other creators is extremely beneficial to your platform more than just to theirs.

As an example, I have totally shifted the way I reach out to other creators. I used to send people a cold message, something to the tune of “Hey, I enjoy your writing….”. Then, I started getting these messages from other creators who wanted to partner with me. And I realized, they were extremely ineffective. Not because I had no interest in partnering with the person, but because if I had never seen the persons name before, it is far more likely that the creator who wanted to partner with me just wanted to use my platform to grow theirs.

If instead a creator liked a few of my notes or had previously commented something insightful under my posts, I was significantly more likely to want to help or partner with that person.

>

Today, before I reach out to any creator I will like a number of their posts and notes and read at least one of their articles and leave an insightful comment under it. This is beneficial to me in multiple ways:

- It creates good will and an instant bond with other writers and transmits a feeling that I actually appreciate their content (which I do).

- It helps me decide whether I want to work with the person or not. Just because an account has thousands of followers doesn’t mean they don’t use AI to think of ideas and write their articles.

- It makes it more likely that the writers reciprocate through liking, commenting and sharing my posts.

If I do decide to reach out to that creator, I will make sure to subscribe before. Some might say that this is a superficial game that isn’t for them, but it’s not. I would argue that I have the more authentic relationship, one built on support and genuine interest rather than just a “how do I gain subscribers mentality”. I end up sending messages only to those creators who I truly enjoy and support, and to the ones I don’t end up sending messages to, I still will like their content. it doesn’t cost me anything and improves their day.

>

If you want to grow your Substack account, be nice to other creators, like their posts and interact with their content.

Tip Three: Learn What Pays Dividends.

Not every investment has an equal reward. This is equally true in business as it is in Substack.

To date, all of my posts combined have brought me a total of 98 subscribers. My top performing (and first ever) note has also brought me exactly 98 subscribers. My posts have taken hundreds of hours of painstaking research, writing and editing. My note took me about 10 minutes to write.

>

Of course, this isn’t the entire picture, but trying to understand the entire picture is overcomplicating things, the main point to take away is a simple one.

>

And therefore it is important to invest your time both in the value you create (your posts themselves) and the outreach you need to do in order to bring people to your page (Notes, Recommendations etc).

The ways to actually grow your user base with minimal work are through notes and recommendations. Recommendations are reliant on your connections with others, notes on your own ingenuity.

I don’t believe that in order to grow through notes you need one of the generic “Dear Substack, connect me with XYZ” notes in order to grow.

But it is extremely important to have notes that are engaging and make people want to view your page. These notes are also a valuable litmus test for understanding what people want to read. If I post a note about a company and it gets zero traction, I know that even if I find the company fascinating, it might not perform well on Substack.

That’s fine and some articles I think are important to write whether or not they are popular - like my piece on Polymarket - but it is nice to know that certain pieces will likely do well. If you want to grow your Substack account, learn what pays dividends.

Tip Four: Lead With Your Heavy Hitters.

When I began this account two months ago, the two most interesting private companies were SpaceX and Anthropic. This had me debating. As the pieces I was planning to write were longer pieces I knew I wasn’t going to be covering the same company in multiple different articles - at least not in a short time horizon.

I was left with a question. Should I write about the most interesting companies first, or start with something slightly less flashy and save those companies for when my subscriber base was bigger? Once my subscriber base was bigger, the post would be more likely to be shared around.

I chose to go with the first option and chose the hottest companies to write breakdowns on. To date, my articles on Anthropic and SpaceX have still been two of my most successful articles, both in terms of viewers and subscribers added. I believe that these posts helped the algorithm push this account and helped me understand that the desire for an account that breaks down the private market is much more than just a niche.

When deciding which post to begin with and in general which post to publish, I believe that leading with your best work is the best way to keep people interested in your work. As time passes and more news comes out, the most interesting company (or thing) yesterday might not be today and I think it is always best to strike when the iron is hot.

If you want to grow your Substack account, start with what is most interesting.

Tip Five: Partner with the right people.

This one is relatively simple, but I believe a lot of people don’t do it right.

Partnerships are an obvious way to grow one’s account - but more than that, they are a way to improve your content.

One of the beauties of Substack is that there are different people with expertise on dozens of different subjects who I can get in contact with.

When deciding who to partner with on a post I am writing, my main priority is the person who brings the most value, not the one who has the most subscribers. This improves my post quality rather than just improving the reach. Of course they don’t have to be mutually exclusive, large accounts are successful exactly for that reason, because they are good at what they do. That being said, when I am looking for someone to partner with on a post, I look first and foremost at which writer would improve the quality of my post, not the viewership.

For me, Learning.Investing.Thriving. has been a gold mine of knowledge. Every time I partnered with him, I felt that I came out with a significantly better post than I would have if I had just done the post myself. For those interested, we worked together on the posts on SpaceX and Polymarket and additionally did a live stream together.

I believe people appreciate this and for multiple reasons.

- Your content is better.

- People understand that when you work with others it is because you truly value their advice, not because you just want to increase your subscriber count.

If you want to grow your Substack account, partner with the right people.

To Summarize:

{kind=link}

The last piece of advice I would have is to just have fun and enjoy the ride. Substack is an awesome platform with tons of good people and it feels significantly more positive than any other platform I have been on.

When you enjoy yourself and connect with other creators who are also writing, you end up learning from these creators. These creators end up giving you tips and advice from their personal experiences that will inevitably help you on your Substack journey. One person who has helped me immensely in this way is Gannon Capital.

It is awesome writing out your own ideas. Both because it causes you to better understand your own ideas and because it forces you to address blind spots in your thesis. In the words of Paul Graham:

>

Additionally, I believe that Substack is still in its growth stage which is awesome. Everyone here is early and being early to anything is usually good!

For those on the fence, I highly recommend starting a Substack. Every person has their unique life story and skillset they bring to the table.

Just be prepared, for those who want to take it seriously, Substack is a part-time job more than just a hobby. While writing is an integral and time-consuming part of growth on Substack, the connections and time spent on the platform are just as important.

Overall, I want to end on a thankful note. Substack has been a wonderful place for me to learn new things, improve my writing, and meet awesome people I never would have connected to without the platform.

u/Roadtochessmaster — 5 days ago

▲ 4 r/Substack

A Full Breakdown: Substack

I wrote a full breakdown on Substack.

It's a bit lengthy but for all those interested in the company, this should cover it all! Hope you all enjoy. Goes over history, valuation, ethical questions and more.

Thank you all! ❤️

––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

One of the greatest benefits of the technological development that has taken place with the internet is the ease of information at your fingertips. Today, information is easier than ever to access and nowhere is this more true than on Substack.

>

Ray Dalio, one of the greatest hedge fund managers of all time, writes on Substack entirely for free. Nate Silver, the elections and sports forecaster also writes his insights on Substack and recently, Thibaut Courtois, long-time Real Madrid goalkeeper and Belgium #1 began to share his thoughts.

Overall, there is a wealth of knowledge on this platform that would make Aristotle jealous. I personally have felt very lucky learning from and making connections with an officer on a polar ice cap, PhD researchers, hedge fund veterans and brilliant writers.

This has all been enabled through a platform which allows its writers to share their knowledge for free with an ability to make money from their knowledge. Today’s breakdown will be on the platform that we are currently using.

The Birth of Substack:

Substack was founded in October of 2017 by three founders with a simple goal.

>

The three founders, Chris Best, Jairaj Sethi and Hamish McKenzie all brought their own unique skills to create a website that gives power to the writers and chooses the user’s mental health over making them spend as much time as possible on the platform.

In our piece on ByteDance last week, we mentioned that Zhang Yiming, the founder of the Chinese media empire wanted to develop the most effective algorithm as possible in order to maximize user retention.

Chris Best, the man with the idea, created Substack due to his frustration around exactly this. Media companies like ByteDance and Instagram were using an algorithm focused on addicting their users. Chris thought that these platforms focused on outrage and superficial content and used advertisements to maximize monetization efficiency.

“These networks compete for users in a war for attention by making systems that spit out superficially compelling content.” - Chris Best in his essay: Two Futures of Media

Chris wasn’t new to founding media companies. He previously co-founded and became the Chief Technology Officer (CTO) at Kik Messenger, a popular platform he helped scale from zero to three hundred million users.

Chris believed that the type of media that was dominating the 2017 landscape was detrimental both to the user and to society as a whole and create a “drug future: a wire to your head that drips dopamine, co-opts your mind, and steals your life.”

Instead of that, Chris left Kik with the goal of creating a different kind of platform. A platform where the network is created in order to best serve its users. A platform where the creators own their audience and choose how to best help their audience. In contrast to other social media companies, writers can choose to pick up and move over to a different platform - and more importantly they can take their audience with them. This is fundamentally different from a platform like Instagram or TikTok, where accounts can be banned and deleted, their audience wiped away forever.

“Creators own their platform, their work, and their connection with their audience. They can make real money and keep the vast majority of the revenue their work brings to the network.”Chris Best in his essay: Two Futures of Media

Substack founders, from left to right, Hamish McKenzie, Jairaj Sethi and Chris Best.

Along with Chris joined Hamish McKenzie - who became the “Chief Writing Officer” a title which he created and is unique to Substack in order to put an emphasis on the importance of writing rather than just general content. Hamish, who previously worked as the Lead Writer at Tesla often notes that he is a writer at heart, rather than a tech founder. A former journalist, Hamish often provides the moral compass that Substack uses including a very pro free speech approach, something we will dive into later in the piece.

In addition, Jairaj Sethi joined and quickly became the behind-the-scenes architect of the whole platform. Jairaj previously worked alongside Chris at Kik as the “Head of Platform and Principal Developer”. Jairaj became the lead engineer and head of product development at Substack, a job he still leads today almost a decade later. Jairaj focused on quickly creating a minimum viable product (MVP) that both allowed users to write articles that were emailed directly to the readers and immediately make money off of that.

Together, they created Substack which instantly became a success. Within a year they had over 25,000 paid subscribers and 150,000 weekly active readers. By November of 2021 Substack had surpassed one million paid subscriptions and a year and a half later in February of 2023, they crossed the two million threshold.

Today, Substack has more than 50 million active subscribers including 5 million paid subscriptions. Substack had 164.5 million monthly visits in April and has now become one of the 250 largest websites in the world by web traffic. Substack now hosts more than 100,000 authors earning money directly through the app including the top ten authors making over $100 million collectively.

Substack best sellers tiers. White for 100. Orange for 1000. Purple for 10,000.

What does Substack offer?

For solo writers, often the hardest part of writing isn’t the writing itself but trying to write while simultaneously managing distribution, payments and growing your audience. Substack offers the whole suite with only a simple fee for those already generating revenue. The huge appeal as a writer is an ability to start from scratch and be able to instantly grow an audience.

Substack is one of the only apps where a creator can begin earning money on day one, without needing millions of impressions or hitting content based milestones. And this isn’t rare on Substack, I myself had my first annual subscriber only a month after I began this account. More than that, I often see people with hundreds of paid subscribers building accounts that turn their fun hobbies into legitimate business operations.

For the readers, Substack offers some of the highest quality in the world, often for free with a twist. If you have been reading on here for a while, you may have noticed a subtle difference between Substack and other social media platforms. The lack of advertisements. While most social media companies have the vast majority of their revenue from advertising - for example Meta had 97.6% of their 2025 revenue come from advertising - Substack uses a business model entirely different.

Substack offers their users an ability to monetize their newsletters and Substack takes a 10% commission on each purchase. For example, if someone upgrades to my yearly plan which costs $200 a year, Substack will take 10% of that or $20 and Stripe (who will be the subject of a future breakdown) takes another roughly 3%. Post fees, the author still receives more than 85% of each subscription while having the ecosystem around them that allows them to flourish.

Product Roadmap:

Besides long-form content like this article, Substack has also moved to other forms of media content moving them from a platform purely for articles to a media app.

Substack added an option for video posts in 2022 and has since continued to expand the ability of creators to upload videos of all types. In 2024, they added Substack shorts, and in 2025 they added swipeable shorts that readers can scroll through. Importantly, these haven’t been pushed to users in the same way that Meta pushes their shorts and truth be told I didn’t know they existed until doing research for this article.

Notes, which launched in 2023, has become an integral part of the Substack ecosystem. Notes allows creators to share short-form content similar to X. Notes is one of the big drivers of subscriber growth and the community feeling as it allows the creator to post daily content and the readers to interact and share their own thoughts as well.

Substack also rolled out livestreams in early 2025 which allows creators to go live, either by themselves or with another creator. In May of 2025, they allowed creators to go live using a faceless option for the content creators who preferred to keep their face anonymous.

With all of these apps, Substack’s goal is to become an all-in-one media company while keeping the emphasis on long-form articles. With video posts and live streams they allow users an alternative to YouTube, with notes an alternative to X and with their articles an alternative to traditional news articles.

The Creator Sphere:

While Substack’s top ten creators make over $100 million a year, it is much less simple for those who are middle of the pack. For those who aren’t at the top of the Substack game, it can be confusing finding the balance between trying to grow and trying to monetize.

Even those who have 100 paid subscribers charging $10 a month - considered by Substack as a best seller - are only making $12,000 before Substack and Stripe take their fees or $10,500 a year after fees, far below the median income for an individual. While Substack isn’t a full-time job, it often takes dozens of hours weekly to research, write, distribute and attempt to connect with other subscribers in order to grow. For those who aren’t best sellers, they are often working in addition to their jobs without any real financial compensation.

Anecdotally, as someone who is now at 1,000 subscribers but has yet to turn on any real type of paywall, it can feel confusing trying to navigate the tension between treating Substack as a part-time passion and a legitimate hypothetical job.

This can often cause burnout when the financial incentive doesn't arrive, creating something called the “Trough of Sorrow" which typically kicks in at two hurdles at 3 months and one year once the hype and excitement cools down.

POV: Continuing grinding on Substack after hundreds of hours of work and three paid subscribers.

TAM:

Substack has a number of competitors, but the more important number to begin with is their total addressable market or TAM.

With every platform, there is a finite amount of users who are interested in that platform or service and with Substack it is no different.

Substack is fighting a greater battle. The battle to move from type one i.e. fast-paced addictive content to type two i.e. slow-paced quality content that leaves the readers more intelligent and fulfilled rather than less.

And so far, they have proven to be a massive success. Substack has fought against the shift towards short-form content and readers on the platform often spending hours reading pieces that make them more intelligent is proof that the website is working. Anecdotally, I can say that Substack went from a platform I hadn’t heard of to one of the main sources of my information in a few short years.

And in a world where the world’s trust in mainstream news is becoming less prevalent among the masses, independent writers and on Substack are perhaps filling the gap of long-form news content. In addition, as mentioned previously, Substack is full of award-winning journalists and writers not just in the politics sphere, but also in business, economics and even one of the greatest chess players of all time, Garry Kasparov.

All this means that Substack’s battle is fighting a two-pronged battle.

- Converting readers that already exist onto their platform.

- Introducing new readers who only know “type one” social media onto a better more insightful platform.

And the readers have been converting, we mentioned some impressive numbers earlier but one that stands out is that Substack added 32 million new subscriptions in only a three month period.

Competition:

As can be inferred from the previous section, Substack’s competition is made up not just of other newsletters, but of social media companies in general. Instagram, Facebook, Reddit and YouTube are all major competitors to Substack, not directly in the newsletter section but as general competition in trying to capture user attention.

Substack also has other competition with other newsletters.

Beehiiv is one of the most popular newsletter platforms specifically for those who are at the top of the Substack game. Beehiiv charges a flat monthly fee similar to a SaaS model depending on the amount of subscribers you have. Importantly, it is not possible to monetize an account on their free plan meaning for the majority of writers starting out without major subscriber bases, they will likely prefer Substack’s free option. Still, Beehiiv is a legitimate competitor especially for those who are Substack’s most valuable customers.

Mailchimp, now an Intuit platform, that has 14,000 users sign up daily is another popular option for those looking to begin a mailing list. Mailchimp is known for their easy-to-use platform that also offers editing tools, built-in AI assistants and helps creators automate their platform. The drawback is again the pricing. Mailchimp’s pricing tier is expensive and charges even for users who are inactive.

Ghost is a non profit open source option that gives creators the full revenue of whatever they earn. Ghost allows you to truly own your platform with the option to customize your website and move your subscriber list and your website whenever you choose. Similar to Substack, Ghost allows you to create tiered subscription tiers and create articles that are only for paid subscriptions. The downside with Ghost is that it is harder to use than Substack and has a smaller profile making growth more dependent on the user than the platform.

Alternatively, for those who are looking for a larger user base, X (previously Twitter) provides a relatively cheap option. The pro in X is that the user reach is massive. X has 561 million monthly active users and over 250 million daily active users. For those only looking to spread their content and reach the maximum possible user base, X is a good option. For premium users, X now has an article feature that allows articles to be posted directly to X. The downside, X monetization is difficult to achieve requiring both a paid subscription and achievement of milestones (5 million impressions + 500 premium followers) in order to qualify. Once qualified, monetization is dependent on the X algorithm rather than the user’s choice. That being said, for those looking for maximum reach, X has around 10x the reach that Substack has.

As you may have noticed, what Substack does best is they offer users a free option that they can immediately monetize together with a recommendations network that helps creators grow quickly. My first paid subscriber came after dozens of hours of hard work but also after zero financial commitment. Substack’s recommendation feature drives 50% of new subscriptions and 25% of new paid subscriptions. Alongside that, notes has become increasingly more popular giving X a space for creators to share short-form content. The combination of free to begin and the ability to grow through the Substack notes and recommendations algorithm makes it an increasingly more attractive option.

The Growing Migration:

>

This is a playbook that is mutually beneficial both for the creators and for the platform and one that is becoming more prevalent as creators realize the value Substack offers.

For the creators, they are able to instantly add another income source and connect to their followers in a more intimate way.

For Substack, each creator who transfers brings a dedicated user base who become engaged users, both with the original creator and likely with other creators as well. In addition, it solidifies Substack’s position as a cash generating bottom of the funnel playbook for creators who have massive followings, creating a flywheel that brings additional creators and users to the platform.

I spoke with two content creators who joined Substack and brought part of their audiences with them.

Trader Joe began his social media career after managing a multi billion dollar fund for a Goldman Sachs spin off. His content was quickly appreciated and he built up a user base of over 250,000 followers across Instagram and TikTok. In February, he joined Substack where he quickly became a bestseller and fantastic source of in depth information.

>

Uninvited joined with a following on both X and a website. While she originally began writing articles on X, she found that she had started enjoying writing on X less and less. She moved to Substack, where she has gained 3,300+ subscribers in only six weeks. She views Substack as a bottom of the funnel platform that she can use in order to go more into niche depths and connect more directly with her followers.

The Ethical Questions:

Every company has its ethical questions and Substack is no different.

With Substack, the biggest question is freedom of speech and how it should be regulated. Substack’s founders are very openly pro freedom of speech but some people believe that they have taken this belief too far.

"Freedom of the press and free speech are not just important but critical for journalists everywhere. Every fight to protect those ideals is worth it." - Hamish McKenzie

The main backlash began in 2023, when Substack was accused of hosting and allowing pro-Nazi and white supremacists to monetize on the platform and benefiting directly from that.

Hamish McKenzie came out and said that the platform “doesn’t like Nazis” and that they wished that “no one held these views” but he importantly didn’t say that removing them from the platform was the right idea. Substack’s initial response was that they would remove accounts who made tangible threats of violence but not those promoting violent ideologies. Substack’s approach was that by removing the extremists from their platform, they would just make the problem worse and draw additional attention to those with extreme beliefs.

>

Hamish McKenzie’s response to writers with extremist views.

Meanwhile, a number of prominent writers came out and said that Substack’s handling of these accounts wasn’t sufficient. Casey Newton, one of the most prominent writers on the platform decided to leave Substack for the aforementioned Ghost, and published a thought-provoking article called “Why Platformer is leaving Substack”. In the article, which I highly recommend, Newton announces his reasons for leaving Substack including saying:

>

Important to note that Newton wasn't leaving behind a small account with some potential. He had thousands of paid subscribers and over 172,000 total subscribers. Additionally, 247 prominent writers signed a letter to Substack asking them to clarify their policy.

Substack ended up banning some of the publication that overtly supported Nazis partially walking back their stance that the best way to strip bad ideas is to subject ideas to open discourse.

Substack is stuck here in a Catch-22, on the one hand, critics of moderation say that freedom of speech should include all opinions.

Freedom only for those who conform to Substack’s views is freedom of agreement rather than freedom of speech.

Proponents argue that as a private platform, Substack is not obligated to follow freedom of speech laws and that the platform shouldn’t be supporting writers that are unethical.

In the end, both sides left unhappy with Substack banning some extreme writers while other writers who were pro-censorship chose to anyways leave the platform.

In addition, Substack has partnered with Polymarket, a problematic prediction platform (read gambling) which is something I covered in depth in my Polymarket article.

Valuation:

Despite the controversy surrounding Substack which caused many writers to leave the platform, Substack continued to grow and more and more writers began newsletters on the platform.

Currently, Substack is not profitable at least as of 2025. This isn’t due to a revenue problem but rather due to an increasing investment into new features.

>

This is a playbook that is common in media companies, Twitter (now X) took twelve years to turn its first profitable quarter.

>

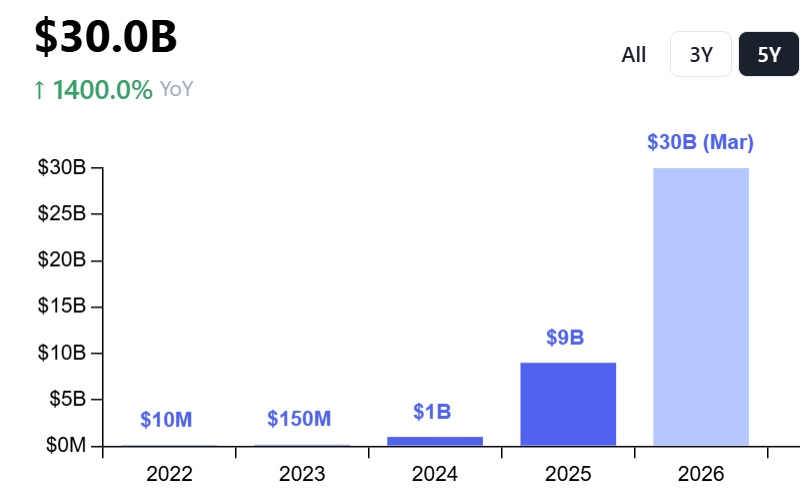

This, along with their revenue growth has caused Substack’s valuation to climb and in July of 2025 they officially crossed unicorn status with their Series C funding round raising $100 million at a $1.1 billion valuation. Substack’s previous Series B funding round had them valued at $650 million in March of 2021 meaning the company grew by almost 70% in slightly more than two years and from zero to $1+ billion in eight years.

When looking at a future valuation and room for growth, it is important to look at valuations of other media companies to understand what the potential could be. Reddit, the online forum app is currently valued at over $32 billion while the New York Times is worth roughly $12 billion.

At a current valuation of $1.1 billion, Substack is still very much at the beginning of its growth stage.

In order for Substack to grow its valuation, it needs to continue growing its users and move from a niche platform for intellectuals to a mainstream media corporation.

The Bear Case:

Creator Emigration:

While Substack is an extremely attractive platform with lots of room for creators, there are a number of downsides that can cause creators to move to different platforms taking their users with them.

First, Substack’s 10% Revenue cut is something that large creators will want to get around. This creates a problem for Substack as it’s most valuable creators have an active reason to leave the platform once they grow their audience. It is also important to note that a creators email list is owned by the writer, not by Substack making migration to different platforms easy for creators who want to move.

This is a phenomenon that has already happened among many of Substacks top creators including Matt Brown who moved his 71,000+ Substack account over to Beehiiv in order to save over $20,000 in fees.

>

Molly White was another prominent Substacker who moved her platform from Substack to Ghost and using some simple “napkin math” demonstrated how expensive Substack can become for those with massive audiences.

Substack does have a major advantage over those platforms namely that the Substack algorithm and recommendations features allow creators to grow at a rate they couldn't when writing through other platforms. Still, for those with huge audiences already, saving tens of thousands of dollars a year can be a big enough incentive to switch over.

In response to major creators switching over, Substack has recently rolled out Subscriber kits which allow Substack bestsellers for creators with more than 100 subscribers. These kits allow creators to directly partner with Substack sponsors and have brand deals come to them as opposed to have to search for them.

Loss of Attention Span:

The other potential bear case for Substack is their TAM shrinking as people become more and more addicted to short-form content like scrolling on Instagram and YouTube. This is something that is already happening. Attention span shrinking is now a fact, not a theory.

>

Substack is fundamentally built around long-form articles which require enormous amounts of attention to consume. When the average person switches tasks every 40-50 seconds, a long-form article with a ten or even twenty minute reading time is becoming more and more rare daily.

In fact, if you are reading this, you are likely one of the few who made it this far and for that, I applaud you.

This is likely one of the reasons why Substack released their shorts feature, but this is far from the core of the platform and actually feels antithetical to why the platform was created.

If Substack’s TAM shrinks, and attention spans continue contracting, eventually fewer people will frequent Substack’s website.

The Moderation Problem:

Another potential downside with Substack is the moderation problem we discussed earlier that caused Casey Newton to leave the platform. I won’t go into it again but Substack is constantly trying to find the balance when performing content moderation that inevitably frustrates both sides.

The Hack:

In addition to the bear case, in February of 2026, Substack announced that they had suffered a data breach in October 2025 that was only discovered months later. The breach importantly didn’t include financial information or passwords and was resolved by Substack only after months of the hackers running rampant with the emails, phone numbers and addresses of nearly 700,000 users.

“It takes 20 years to build a reputation and five minutes to ruin it”

Warren Buffett

With the breach, Substack users had their data exposed for months without their own knowledge, a fact that is particularly worrisome. Included in those breached were government officials and journalists. Importantly, while the email was leaked, it was not leaked with the password meaning user’s emails themselves weren’t compromised.

With the advancement of AI models like Anthropic’s Mythos, data attacks will likely become easier for individual users to partake in. The fact that Substack already had a major data leak in a world that is becoming more and more dangerous is worrisome to say the least.

In Substack’s defense, these types of leaks happen relatively often among top companies and are considered standard costs of using the internet. Yahoo had three billion in a four year long data leak, Meta had 500+ million users have their data leaked and even Marriott International had the information of up to 500 million guests leaked.

The IPO and Final Thoughts:

Substack currently doesn’t have any near term plans to IPO. Their most recent Series C funding round which was led by BOND and The Chernin Group now gives them ample capital to work with.

For now, it seems like Substack is focused more on private funding and growing the platform rather than going public and having to deal with the headaches of life as a public company which include investor calls, additional financial scrutiny and short term investor pressure.

With its most recent funding round and its entry into unicorn status, Substack has officially stopped being a small media company and has officially become a website recognized for its use and influence. That being said, it is still early in its growth process and likely will want to become profitable and increase its user base before considering an IPO.

On a personal note of gratitude, I want to thank Substack as a platform for providing me a platform to write and share, to grow and flourish. Substack might not be perfect, but their monetization structure makes it free to start and to grow and for that I am thankful.

To the readers, thank you for reading my work, your support means the world to me.

u/Roadtochessmaster — 16 days ago

▲ 0 r/sui

Full breakdown of ByteDance

Hey All!

I spent the last while researching ByteDance including speaking to a Chinese lawyer to understand China more properly. Usually the pieces I write are 20-25 minutes but I know those on Reddit enjoy shorter stuff so here's the TLDR: Would love to hear thoughts!

TLDR:

- ByteDance isn’t one or two apps, it’s dozens of different apps that dominate both in mainland China and abroad. It is in every way a media empire the same way that Meta is.

- ByteDance’s revenue growth is one of the fastest in the entire world at the scale they are at. They went from being less than a quarter of Meta’s revenue in 2019 to being almost equal only six years later. This is despite Meta’s 18.5% revenue CAGR over the past five years.

- Operating in China isn’t like operating in the US. Both domestically and internationally, ByteDance has major complications that arise and they constantly have to toe the line between pleasing their own government and not offending international ones.

- ByteDance’s valuation is affected just as much by external geopolitical factors as it is by the financial ones. It therefore has a current estimated valuation significantly lower than it would if it were operating out of Silicon Valley.

- ByteDance is investing extremely heavily into AI and currently boasts China’s leading chatbot: Doubao.

- Overall, fascinating company and likely undervalued because of the geopolitical reasons. I would stay away for ethical reasons.

Joseph

For those who want to read the full piece, enjoy below!

u/Roadtochessmaster — 25 days ago

▲ 5 r/IMadeThis

Feature your startup.

I write on Substack about private companies. Currently have 1100+ subs in the last month and a half.

So far I’ve been focused on larger private companies, SpaceX, Anthropic, ByteDance etc.

Was thinking it would be cool to potentially hear first hand if anyone has a startup or something they want to pitch. My articles are in depth, garner between 600-1000 views usually. Would also be interested in potentially doing a live stream.

Would love to hear thoughts!

Joseph

Edit: Figured it might be relevant to link the publication.

https://preipomedia.substack.com/?utm_campaign=profile_chips

u/Roadtochessmaster — 25 days ago

▲ 0 r/TikTok

Full breakdown of ByteDance

Hey All!

I spent the last while researching ByteDance including speaking to a Chinese lawyer to understand China more properly. Usually the pieces I write are 20-25 minutes but I know those on Reddit enjoy shorter stuff so here's the TLDR: Would love to hear thoughts!

TLDR:

- ByteDance isn’t one or two apps, it’s dozens of different apps that dominate both in mainland China and abroad. It is in every way a media empire the same way that Meta is.

- ByteDance’s revenue growth is one of the fastest in the entire world at the scale they are at. They went from being less than a quarter of Meta’s revenue in 2019 to being almost equal only six years later. This is despite Meta’s 18.5% revenue CAGR over the past five years.

- Operating in China isn’t like operating in the US. Both domestically and internationally, ByteDance has major complications that arise and they constantly have to toe the line between pleasing their own government and not offending international ones.

- ByteDance’s valuation is affected just as much by external geopolitical factors as it is by the financial ones. It therefore has a current estimated valuation significantly lower than it would if it were operating out of Silicon Valley.

- ByteDance is investing extremely heavily into AI and currently boasts China’s leading chatbot: Doubao.

- Overall, fascinating company and likely undervalued because of the geopolitical reasons. I would stay away for ethical reasons.

Joseph

For those who want to read the full piece, enjoy below! - https://preipomedia.substack.com/p/the-breakdown-bytedance

u/Roadtochessmaster — 25 days ago

▲ 0 r/biotech

A Breakdown, Isomorphic Labs

Hey Guys!

Took some time writing about Isomorphic Labs, hope I did it justice. In order to properly understand the company, I spoke to two biotech researchers, and an executive at a biotech company. The article is lengthy, included a TLDR for those who don't have 15-20 minutes.

TLDR:

- Isomorphic Labs is a fascinating interesting company focused on using AI to "solve all disease".

- Spin off of Google's DeepMind, the founder of the company Demis Hassabis is brilliant and carries a valuation multiple to his name. (Whether he should or not is a larger question I address in the piece).

- With massive funding from Google and two sovereign funds, Isomorphic Labs has a big advantage in a capital heavy industry.

- Massive Funding ≠ Success, the biggest sign looking forward will be human trials, scheduled for end of 2026.

-------------------------------------------------------------------

>“Drug discovery is a messy problem. It can take upwards of a decade to get a drug all the way from the initial stages of a project all the way through onto the market…. 90% of compounds that enter the clinic don’t come out the other side. The whole process can cost up to $3 billion.” - Rebecca Paul VP, Head of Drug Design, Isomorphic Labs

What if a company could use AI to fundamentally reinvent the drug discovery process? Make it more effective, cheaper to develop and significantly speed up the process. What if the company was founded by a Nobel Prize winner in chemistry? What if this company was a spin-off of Google’s DeepMind? What if you could combine them all together and create one company?

Enter Isomorphic Labs.

Isomorphic comes from a Greek term. It describes two things that are similar or identical in structure even if the outer appearance differs. Isomorphic Labs believes that AI and biology are isomorphic and that frontier AI can “unlock deeper scientific insights, faster breakthroughs, and life changing medicine.”

Today, Isomorphic Labs is at the forefront of the AI medicine synergy. Their goal, of “solving all disease” may sound far-fetched, but with huge funding from Google as well as the sovereign funds in the UK and Singapore, they are no longer just a pipe dream. Their partners include companies worth hundreds of billions of dollars including Eli Lilly and Novartis. Human trials are expected to take place in late 2026, potentially moving Isomorphic Labs from the theoretical to the real world and provide a real indicator of whether AI can fundamentally change the way that drugs are developed.

By way of a roadmap, this piece will begin by talking about the founding of Isomorphic Labs, and its origin story. We will then continue by explaining what AlphaFold is and how it revolutionized the biotech world. After that, we will explain what Isomorphic Labs actually does, its current partnerships today and look at the founder of the company and assess how a celebrity founder affects the company. We will then continue looking at the company itself and the main question surrounding it, before looking at the TAM, competition and valuation. I will then discuss a potential IPO date and give my final thoughts on the company. This is a fascinating company even for those who don’t frequent the biotech space. Enjoy 😄

The Birth of Isomorphic Labs:

In 2014, Google acquired DeepMind. Their goal was to “Solve intelligence. Use it to make the world a better place.”

And while they haven’t exactly solved intelligence, they have made massive strides using artificial intelligence to make the world a better place. In 2020, DeepMind developed AlphaFold2, a protein folding breakthrough where they used AI to map 3D structures of virtually all known proteins. By understanding protein structures in greater detail, scientists are able to better design targeted drugs that can solve previously unsolved diseases. Think of proteins as the blueprint of the human body. If you can understand the blueprint perfectly, you can find what is working properly, and what is broken and needs to be fixed.

In 2021, spurred by the success of the AlphaFold2, Google’s DeepMind spun off Isomorphic Labs with the goal of “solving all disease.” The head of the company was the same Demis Hassabis who would go on to win a Nobel Prize for the protein folding breakthrough.

Spinning off Isomorphic Labs from the original DeepMind project allowed it to focus on the highly regulated world of drug manufacturing rather than be an additional biotech project in an AI research laboratory. In addition, drug testing is both extremely expensive and carries a near 90% historical failure rate. Spinning off Isomorphic Labs allowed the company to focus and hire on recruiting biology experts while not having the high capital expenditure costs on DeepMind’s balance sheet. Importantly, Google is still massively invested in the company and likely has voting power to make the key decisions as they see fit.

AlphaFold, the Breakthrough.

Isomorphic Labs’ goal is to solve all disease. And in order to do that, they are using AI to rapidly speed up the process. In fact, according to Max Jaderberg, the president of Isomorphic Labs, in a few years, drug design will be synonymous with AI.

>“In five years time, doing drug design without AI will be like doing any sort of science without math… If you are not using AI, what are you doing.” - Max Jaderberg.

But before we get to that, we have to backtrack a little bit.

The human body is made up of around 20,000 protein-coding genes. These proteins combine to create about 80,000 to 400,000 unique protein variants. Everything in the human body comes down to these proteins and how they mutate. Hypothetically, if you could perfectly map out every human body and understand how proteins interact, within it, medicine would be transformed. Scientists could detect diseases earlier and potentially even send deadly diseases into remission, create side effect free cures and even go a step further, and reverse human aging. While biology is far more complex than simply proteins alone, protein structures are very useful for rational drug design and the ability to look at a protein and create a drug that fits - almost like a jigsaw piece in a puzzle.

Of course, this is much easier said than done and until a few years ago, working out the structure for one single protein would take months or even years. To complicate matters, each one of these proteins has a unique three-dimensional structure that it can fold into.

The release of AlphaFold in December of 2018 revolutionized the entire field. It essentially used AI to understand and map out highly complex three-dimensional shape. AlphaFold was able to predict protein structures with 90% accuracy, matching human laboratory techniques in seconds, rather than years. All in all, AlphaFold was able to predict the structures of 360,000 proteins. With the release of AlphaFold2, DeepMind successfully mapped out virtually all 200 million known proteins.

>Think of it like any other AI - ChatGPT/Claude etc. Except instead of being trained on language and text, AlphaFold was trained on data - specifically structural biology data collected over decades and decades of biomolecules. - A Biotech Researcher

Scientists instantly used this to make breakthroughs in health. A liver cancer that targeted a protein had no known protein structure and therefore made traditional drug design very difficult. Then, in a collaborative project, an AI drug-discovery company partnered with AlphaFold2 to understand the protein. AlphaFold2 generated an extremely accurate 3D model and within 30 days the scientists custom designed a “hit molecule” to fight the cancer. For some context, this is an unheard of timeline in pharmaceutical drug discovery, and it was only made possible through the use of AI.

In pure numbers, AlphaFold is revolutionary. In 1962, John Kendrew and Max Perutz won the Nobel Prize for mapping the first two protein structures. Then, for the next fifty years, tens of thousands of the brightest scientists revealed the structures of 150,000 proteins, the grand sum of human effort. Then, came AlphaFold. In a few years, AlphaFold was able to predict the structures of 200,000,000 proteins.

A picture released by the DeepMind team of a 3d structure of a protein.

Demis Hassabis and John Jumper won the split 2024 Nobel prize in chemistry for their breakthrough advancements “for protein structure prediction.” This is just the beginning and with the release of AlphaFold3, a model that is significantly more efficient than AlphaFold2, the team at Isomorphic Labs is hoping to revolutionize medicine and drug development.

>“The modelling capacity are getting significantly more sophisticated with every release. The size and complexity of the run is greater and takes less time. With AlphaFold2 it took me about 13 hours to run 2 proteins with a combined total number of amino acids of around ~2000. I had to wake up at night to make sure my computer monitor didn’t turn off. Now in half an hour I can run around 10,000 amino acids in multi-protein complexes. - A Biotech Researcher

It is important to note that as great as AlphaFold is, at the end of the day, it is just a model, not real experimental data. The difference is like a photograph i.e., a real experimental structure, and a drawing i.e., AlphaFold’s prediction. It’s a model based on information predicted about an object, and not a photo of the object itself. Often they are pretty close or spot on - but there’s a limit to how much a biologist would trust it. Think no matter how accurate a painting of a jungle is, it’s not as accurate as a photo of someone in the jungle.

What Does Isomorphic Labs Do?

“Make me a drug for X disease, off it goes, here’s the molecule… Do you think that’s possible?” “It’s possible…Everything is pointing in that direction.” Max Jaderberg, President of Isomorphic Labs

Notably, AlphaFold2 wasn’t developed by Isomorphic Labs rather by its sister company Google DeepMind. DeepMind chose to release its code and model to the public, something that allows science to develop and advance. It also helped established DeepMind as one of the world leaders in AI.

While AlphaFold2 - and subsequent models - aren’t unique to Isomorphic Labs, Isomorphic Labs is using that technology to build their proprietary models. Because they are currently in the first stages of development in a field that is extremely regulated, they currently have not treated anyone or even gotten to the trial stage yet. That being said, the first trial runs are supposed to be in late 2026. Medical trial tests are often pushed back, and the first human trials were originally set for the end of 2025 before being pushed back.

The end goal, will be to use AI to make drug research more efficient. This can come in many different forms including figuring out how drugs will react with proteins in the human body, discovering new therapeutics that were previously thought impossible to target and speeding up the current decade long trial and error process into a few years or even months.

The current market standard that Isomorphic Labs is trying to improve.

Partnerships:

And today, Isomorphic Labs is partnering with some of the biggest names in the pharmaceutical industry. They initially partnered with Novartis - a Swiss pharmaceutical company worth $250 billion - in January of 2024 focusing on the “discovery of small molecule therapeutics against three particularly challenging targets.” After a year, both sides decided to expand the partnership in February of 2025.

“Over the past year, we have witnessed the exploration of new chemical spaces that would be unavailable to probe through traditional methods.” Fiona Marshall, President of Biomedical research at Novartis.

They have also collaborated with Eli Lilly (the American pharmaceutical giant that just passed a $1 trillion market cap) and Johnson & Johnson. These partnerships help Isomorphic Labs in multiple different ways that are crucial to a young company.

- These pharmaceutical giants give Isomorphic Labs access to additional resources and decades of data that they wouldn’t be able to access otherwise. This data can then be used by Isomorphic Labs in order to validate that their work is truly groundbreaking.

- These partnerships also give them significant capital with which to work with, something that for a startup with no revenue is vital. Partnering with other companies also allows them to broaden the scope of their research, allowing them to deploy their technology to a wider variety of therapeutic areas than they would be able to pursue alone.

These partnerships usually involve upfront payments with bonuses that are contingent on hitting milestones. The partnership with Lilly included $45 million in cash upfront and future payments that reach up to $1.7 billion. The Novartis deal was also huge, with $37.5 million upfront and another up to $1.2 billion dependent on results. While the J&J deal was confidential, we can assume that the deal also included a large sum, with the deal likely ranging from hundreds of millions to billions of dollars.

Possibly one of the strongest forms of validation that Isomorphic has is that these companies are customers, rather than investors. These massive pharmaceutical giants view these as partnerships, rather than venture capital investments. For those who believe in Isomorphic Labs, the big pharma stamp of approval is a hugely positive sign. Investment requires a belief in an idea, customers require a product that provides value.

The Demis Factor:

One of the most important parts about early startup companies is the leadership. And with Demis Hassabis leading Isomorphic Labs you can be sure that the leadership is capable and innovative.

That being said, Demis Hassabis, as capable as he is and despite winning the Nobel prize in chemistry, is not a chemist by trade.

Demis Hassabis accepting his share in the winning of the 2024 Nobel Prize in Chemistry.

Demis was born in 1976 and quickly became a chess prodigy. By 13 years old, he was a chess master, at his peak ranked second in the world for his age gap ranked only behind Judit Polgar, who later went on to become the greatest female chess player ever. He then went on to become a video game and AI programmer before studying computer science at Cambridge. After almost a decade of work in neuroscience, he got his PhD in neuroscience before co-founding DeepMind. His work with DeepMind revolutionized many fields, and with the release of AlphaFold and its subsequent models, he fundamentally altered chemistry research. While all incredibly impressive, none of these are inherently chemistry achievements.

Which leads to the next point, there can also be a downside when it comes to having a “celebrity” name as the founder of a company. Namely, the valuation outpacing the actual products of the company. Demis carries a weight behind his name that likely has helped Isomorphic Labs raise $2.7 billion in funding.

The Big Question:

The biggest question mark with Isomorphic Labs is whether or not their technology will work. Artificial Intelligence is fundamentally changing the way many fields operate, but it is not fully clear that AI will fundamentally change drug production.

Chess was for a long time considered one of the peaks of human intellect and for a long time it was unclear whether artificial intelligence would even be able to beat humans. Then, in 1997, the AI model Deep Blue beat Garry Kasparov, at the time, the number one chess player in the world. And since then, artificial intelligence has significantly improved to the point where today, any AI model can easily beat the best player in the world.

But biotechnology might be fundamentally different than chess. While chess has a finite amount of pieces, with biotech and drug production, there are always unknown factors when it comes to protein binding. Drug design could be compared to chess, but chess in which there is a random mystery piece whose behavior you don’t know.

It is therefore unclear whether AI will learn at a pace that will shoot past humans in terms of their ability to develop drugs.

And that is one of the reasons why it’s not clear that Isomorphic Labs will work. Despite raising $2.7 billion, Isomorphic Labs has not dosed a single patient.

And in the meantime, the human trials that were supposed to have begun in 2025 have been pushed back. Currently, human trials are supposed to begin towards the end of 2026 although it is very possible these get pushed back as well. For Isomorphic Labs, so much hinges on this one question. Until an AI company is able to actually dose a human with their product, the potential revolution will always remain just a promising theory draining capital.

>“There is a lot of doubt in the traditional academic & biotech research community that the answers to fundamental biological questions can simply be brute-forced given enough compute. Our understanding of seemingly simple concepts such as protein structure nevermind function is actually extremely limited and shaped by just a few decades of gradual progress.The concern is that biology is being over-simplified and treated as a pure data analysis

problem.

At the end of the day working in Biotech requires facing a harsh reality that can't be circumvented nearly as easily as in Computer Science: things either work or they don't. In the case of Isomorphic, their core thesis is that they can accelerate the speed of drug discovery and development using AI. As long as they do not have at least one drug candidate in clinical trials (and they're late on their initial targets), that thesis remains quite uncertain.” An unnamed executive of a biotech company.

Investments From Other Companies:

One of the most exciting things behind Isomorphic Labs is the amount of money backing it. In a field that often requires massive amounts of capital, having backing from a trillion dollar company and multiple sovereign wealth funds could be the difference between failure and success.

As mentioned previously, Alphabet (the parent company of Google) has a massive investment in Isomorphic Labs. While the amount isn’t public, Google likely has between hundreds of millions of dollars to a billion + invested in the company.

Sundar Pichai giving a presentation introducing AlphaFold-3

And they aren’t the only ones who are heavily invested in the company. Recently, in May of 2026, Isomorphic Labs announced that they held funding round that raised $2.1 billion. The funding round was led by Thrive Capital, who is famous for its high conviction bets. Thrive has famously invested in a huge number of winners, including Instagram at a $500 million valuation and Spotify at a $3 billion valuation. More recently they have invested heavily into SpaceX at a $38 billion valuation, Stripe at a $3.5 billion valuation and OpenAI at a $29 billion valuation. Having Thrive as a backer is huge bet from a firm that has had numerous successful ones in the past few years and is a huge stamp of approval from a major player in the private industry.

And in that round, two sovereign funds and a foreign investment fund have also decided to invest. The UK Sovereign AI Fund, Temasek, Singapore’s state owned investment firm and MGX, an investment fund based in the UAE, decided to invest in Isomorphic Labs most recent funding round.

No company is too big to fail, but these additional investments from sovereign funds and MGX prove that Isomorphic Labs isn’t just one of Alphabet’s fun side projects. And Alphabet actually has a history of being able to turn futuristic technology into businesses worth billions. In November 2022, famous billionaire investor Chris Hohn said this about Waymo: “Waymo has not justified its excessive investment and its losses should be reduced dramatically”. Today, a few years later, Waymo is now worth $126 billion, roughly four times what it was worth in late 2022.

Total Addressable Market (TAM) and Competition:

Looking forward, the biotech/AI industry is one that will almost certainly expand. And therefore, they will be excellently positioned to continue growing as more investment continues pouring in. Furthermore, in a potential winner take all field, Isomorphic Labs is ahead of their competition in funding with an extremely capable staff and a huge war chest behind them.

Isomorphic Labs immediate TAM is in the AI drug discovery market, valued at $2.35 billion by Grand View Research. However, it is a market that is projected to grow quickly, to $13.77 billion in 2033, a 24.8% CAGR. Isomorphic Labs, through its proprietary IsoDDE (Isomorphic Labs Drug Design Engine) is positioned as one of the key players in this field going forward. With the massive deals mentioned previously, they are no longer a fully speculative play.

But there is a larger potential TAM that Isomorphic Labs could transition into. Namely, Pharma R&D. Currently, there are over 23,000 drugs in development being developed by over 7000 companies. Global pharmaceutical spend on R&D reached $306 billion in 2024. In 2025, Johnson & Johnson alone spent $14.7 billion on R&D.

Roughly one third of this spend is on the pre-clinical discovery phase. And AI has already proven to help speed up this process.

AI has demonstrably improved preclinical success rates. It has not yet cracked late-stage efficacy.”

With their deals with Novartis and Lilly, Isomorphic Labs has already managed to break into this market. Notably, while there is an upfront payment included, the vast majority of the total $3 billion deal is tied to milestone achievements, potentially showing uncertainty among big pharma and confidence among the Isomorphic Labs teams.

And this is an area that desperately needs something new to make it more efficient. Despite massive progression in technology and the tools available, today, fewer drugs are being approved per dollar than in the 1960’s, even adjusted for inflation. This is often called Eroom’s law in the pharmaceutical world.

The number of new drugs approved per billion dollars of R&D spending has halved approximately every nine years since 1950…. This dynamic is why AI is not optional. When a single Phase 3 failure can erase $500 million in sunk cost, any tool that improves early-stage prediction of clinical failure has compounding value.

This means that pharmaceutical companies will be looking closely at AI to see if it can speed up the process or increase efficiency in any way. And Isomorphic Labs leads this field.

The last possible TAM that isomorphic could target is the largest of all, the entire global therapeutics market valued at over $1.6 trillion in 2025. If Isomorphic Labs could hypothetically develop, market and sell their own drugs, (with possible partnerships with big Pharma), they could address a much larger market. While this is the largest potential market, it is also the furthest away. That being said, Isomorphic Labs bull case does not rely only on this market, rather any of the potential three TAM cases working out.

In the meantime, Isomorphic Labs is not the only company in the AI/Biotech world. Insilico Medicine is already public with a $22 billion market cap, with a goal to “extend healthy, productive longevity for everyone by using generative AI to transform drug discovery and development”. They aren’t alone, Schrödinger, Recursion Pharmaceuticals, and Exscientia are all using AI to try and advance pharmaceutical research.

What Isomorphic Labs has that differentiates itself from competition is a unique ability to use AlphaFold. When DeepMind released AlphaFold to the public, they also enacted strict non-commercial terms. As a sister company to DeepMind, Isomorphic Labs is the only AI Biotech company that can use AlphaFold’s technology to commercially. Competitors are trying to reverse engineer alternatives as quickly as possible, but AlphaFold truly is revolutionary.

That doesn't guarantee success above all competition. While a lot of the numbers mentioned in this section seem super promising, again it is important to remember that none of these numbers matter if Isomorphic Labs is unable to produce successful clinical drugs. In the meantime, their competitors are rushing ahead. Insilico Medicine has already dosed dozens of volunteer patien

Ethical Questions:

Surely with a company developing drugs to cure people there are no ethical questions… right? Not exactly.

With any new technology, ethical questions are bound to arise. With Isomorphic Labs it is no different. While the general goal of the company is extremely noble - solve all disease - that doesn’t inherently mean that every company in the field is noble.

“Even if all the actors are good in that environment, let alone if you have some bad actors, that can drag everyone to rush too quickly, to cut corners.” - Demis Hassabis

If biotechnological advancement come into the hands of the wrong actors, it could cause immense destruction. With generative AI, someone could hypothetically design toxins that commercial screening would not notice. Unfortunately, this is no longer a hypothetical as in October of 2025, the “Paraphrase Project” confirmed that screening is only 97% accurate. With something as potentially harmful as biochemical toxins, having a generative AI that could create toxins or even biochemical weapons, is leading us towards a dangerous and scary world. And the risk is real, even if 99% of the world is moral, even a few bad actors could cause immense and irreversible damage.

Future Revenue and Valuation:

After their most recent $2.1 billion funding round, estimates for the valuation of Isomorphic Labs ranges between $10-12 billion to $15-20 billion. In either case, they have passed the $10 billion threshold and are no longer a small cap company. Perhaps more importantly, they are by far the largest AI-biotech company. If this is an industry that will prove to be successful and grow long term, Isomorphic Labs will be primed to grow rapidly as investment pours in.

If Isomorphic Labs is able to scale and pass the human trials stage, they will have a few main streams of revenue.

Usually, with pharmaceutical research companies, the primary cash influx comes in the form of selling the drug or treatment they built to big pharma. The company then gives pharmaceutical companies the bulk of the profits, while they generate a small royalty commission on each sale. This gives them a one time influx of capital which research companies rely on after a capital draining trial process and a long term stream of income. However, because Isomorphic Labs is backed by the massive war chest that is Google, they don’t necessarily need the massive immediate payment. They could therefore hypothetically only sell part of their ownership for strategic reasons and maintain a larger percent of the ownership.

The benefit with partnering with big pharma goes beyond just the one time payment and royalty fees. By partnering, Isomorphic Labs use the massive resources available to big pharma companies in order to push their products out to market. This allows Isomorphic Labs to focus on production rather than distribution.

Another way of generating revenue would be researching, developing and producing their own drug. As mentioned previously in the TAM section, this is the hardest but highest-reward play. By doing this, they transition from a AI biotech research company to a full fledged competitor to big pharma.

The IPO date.

Often, biotech companies will go public due to the immense costs associated with developing drugs. However because of Isomorphic Labs unique position with backing from both Google as well as multiple sovereign funds, they don’t need to go public anything soon. Therefore, for those interested in investing in them privately, this will be a very long term hold where your capital will likely be illiquid.

This doesn't imply that Isomorphic Labs is a bad bet. A few years ago, someone investing in Anthropic was investing in an AI company burning through cash in an unproven field. Today, that same investment is likely worth magnitudes more than it originally was. That doesn’t mean that investing into every AI “startup” is advised, investing should always be treated with caution, especially in the private market where fees are usually higher and illiquidity is often the case.

For retail investors without the ability to invest in private companies, the best way to invest into them likely remains investing in their parent company, Alphabet. While Google is so massive that Isomorphic Labs is only a tiny sliver of the companies overall valuation (probably around 0.1%), this is the only direct way to invest in them. If Isomorphic Labs does turn into a trillion dollar company, the value of Google’s stake in them will grow exponentially.

>“Isomorphic is not a buyout target, it is the engine everyone else wants to rent. Lilly, Novartis, and Johnson & Johnson are all paying upfront plus billions in milestones just for access to the platform. With Alphabet holding the majority stake and roughly 2.6 billion dollars raised across two Thrive-led rounds, this looks far more like a future landmark IPO than an acquisition. The catalyst to circle is the first human trial, expected in late 2026. The day an AI-designed molecule gets dosed in a person, the whole category re-rates.”

Final Thoughts:

Google clearly has a huge conviction in Isomorphic Labs, which is why they have invested hundreds of millions or more in the company. Through partnerships with some of the biggest pharmaceutical companies, Isomorphic Labs could potentially rerate and the valuation could shoot up, proving another successful spin off by Google.

Isomorphic Labs has a lot of confidence in the statements that they have made. But the idea of “solving all disease” is currently still decades away,

However, there is another possibility, that the AI biotech space is now disconnected from the actual reality. That a company with zero dosed patients shouldn’t have billions of funding poured into it because of a hope. If so, we are likely watching capital dump into a company destined to fail. Modeling protein structures is one thing, solving all disease is another.

I don’t have a position in Isomorphic Labs, but for the sake of humanity I hope the company succeeds. Demis Hassabis released AlphaFold to the rest of the world instead of keeping the technology proprietary because that was what would do the most good for society. If Isomorphic Labs really can even partially succeed in their main goals, the world will become a better place, and for that reason, I hope they do.

“One day I hope we will be able to reduce drug discovery down from taking like ten years on average to go from understanding a target to having a drug in the clinic to maybe a matter of months or even weeks.” Demis Hassabis.

u/Roadtochessmaster — 1 month ago

▲ 8 r/Substack

Substack Growth Has Stalled

My substack was flying for the first month, all of a sudden it suddenly feels like my growth died.

Did anyone have this?

I see with my notes that none of them are getting the same traction they previously did.

I’m about 35 days in, my niche is private companies.

Anyone have any advice?

u/Roadtochessmaster — 1 month ago

▲ 0 r/biotech

Research into Isomorphic Labs

Hey all! I write articles on private companies, and I have stumbled upon the biotech world.

Writing an article on Isomorphic Labs now, I spoke to someone who has a PhD in biochemistry for over an hour who was super helpful in helping me understand the company and the larger biotech world in general.