u/Optimal_Image5192

▲ 2 r/StockMarket

Canaccord Analyst Initiates Coverage on $INFQ with a Buy Rating and PT of $22/Share

"We are initiating coverage of Infleqtion with a Buy rating and a $22 price target, implying ~70% upside from Wednesday’s close. Every qubit fights the same battle: holding a fragile quantum state together before heat, vibration, or measurement itself destroys it.

Quantum computing is a war against entropy. Infleqtion, like everyone else, is engaged in that war, but it also does what no public peer can: it sells the other side. The same environmental sensitivity that ruins a qubit makes a quantum sensor exceptional, and Infleqtion monetizes it today through atomic clocks, RF receivers, and inertial navigation sold into defense and aerospace. Infleqtion’s dual model anchors our Buy.

We like the Infleqtion story for four key reasons: INFQ’s neutral atom approach offers compelling scaling and error-correction flexibility. Neutral atoms have practical advantages. Scale is achieved by trapping more atoms with lasers, not by fabricating more chips, so growth is an optics-and-control problem rather than a manufacturing-yield one. Every atom of a given element is exactly identical, so unlike solid-state qubits there is no chip-to-chip variation to engineer around.

Sensing is a key differentiator and a primary beneficiary of the June 22 executive order. Infleqtion is one of very few public names with a commercial sensing portfolio across timing, RF, and inertial navigation, with live defense programs across all three AUKUS partners, a first-of-kind Tikker demonstration aboard a Royal Navy uncrewed submarine, and a NASA Cold Atom Lab supplier relationship.”

- Analyst: Kingsley Crane

u/Optimal_Image5192 — 4 days ago

▲ 16 r/sp500

META IS BUILDING A CLOUD BUSINESS TO SELL EXCESS AI CAPACITY!

$META is reportedly developing a cloud business to sell access to excess AI compute, per Bloomberg.

The internal initiative is called Meta Compute.

The plans being considered:

AI model access hosted on Meta infrastructure, similar to AWS Bedrock

Raw AI compute capacity, closer to CoreWeave

Developer access to Meta’s data centers, chips, and models

Napkin math for potential revenue here for META:

1GW of compute capacity

$20B revenue per GW

$20B total revenue

85% operating income margin

$17B operating income

$14.6B net income

$5.69 EPS

16.3% accretion to FY27 consensus EPS

u/Optimal_Image5192 — 5 days ago

▲ 49 r/StockMarket

$OKLO Announces D.O.E. Approval of the Documented Safety Analysis (DSA) for the Groves Isotope Test Reactor in Texas

$OKLO's Groves Isotope Test Reactor received DOE approval for its Documented Safety Analysis.

This is the final safety basis approval that follows the earlier Nuclear Safety Design Agreement (NSDA, approved March 2026) and Preliminary Documented Safety Analysis (PDSA).

With the DSA now approved, the project shifts from the documentation/design-construction phase into DOE’s final pre-startup activities: readiness review, startup approval, fuel loading, and first criticality.

Oklo is targeting July 2026 for first criticality.

CEO Jacob DeWitte highlighted that Groves is the first advanced reactor project to receive DSA approval on privately owned land.

The Groves facility is essentially a pilot project focused on domestic isotope production for medical (cancer diagnostics/treatment), industrial, research, space, and national security uses. It aims to reduce reliance on overseas or aging sources while generating operational data to support future commercial reactors.

u/Optimal_Image5192 — 5 days ago

▲ 17 r/StockMarket

$QCOM Investor Day Highlights Their Strategic Pivot to AI Infrastructure

Qualcomm $QCOM plans to bring parts of its new data-center chip architecture to smartphones, PCs and cars, per Semafor.

Their High Bandwidth Compute architecture stacks memory & compute vertically to improve data flow, potentially enabling more local AI models and always-on agents on mobile devices.

Based on their investor day presentation, it seems to me like they’re aggressively diversifying away from their traditional smartphone (handset) chips business to becoming a broader AI platform company across the entire compute spectrum imo. This includes on-device inference/edge AI to data centers, automotive, industrial systems, robotics, etc.

This is expected to drive massive new demand for efficient inference compute, both on devices (personal agents) and in data centers (scaling those agents), plus “physical AI” in cars, robots, and factories. They announced huge diversification targets including $40B non-handset revenue by FY29 (up from $22B prior), over $15B from data center AI by FY29, $5B data center revenue in FY27, and EPS above $18 in FY29.

According to $QCOM, the combined TAM for these opportunities is roughly $1.7 trillion by 2030. Important to note that these are long-term targets (not immediate quarterly guidance). They reflect management’s view of secular tailwinds from distributed AI compute over the next 3–5+ years.

u/Optimal_Image5192 — 8 days ago

Samsung Validates Hybrid Bonding’s Clear Advantage in HBM4E Thermals

A Korean tech news outlet (ET news) published the article today, June 25, 2026, reporting that Samsung had published their research (an IEEE paper titled “Analysis of System-Level Thermal Characteristics of Hybrid Cu-Bonded HBM with 2.5D Advanced Packaging”) showing the thermal management advantages of their Hybrid Copper Bonding (HCB) technology over traditional Thermo Compression Bonding (TCB) for next gen HBM4E memory.

Samsung’s HBM4E and hybrid bonding plans already existed with HBM4E and Hybrid Copper Bonding (HCB) tech showcased at Nvidia GTC in March 2026, but this system-level thermal validation from the IEEE paper is new and exciting to me. In the IEEE study, they used multi-scale modeling and test chips in server-like conditions. They showed clear benefits like lower hotspot temperatures, reduced thermal interference between memory stacks and logic, more than 15% thinner stacks, and better power budgets for 16+ layers of HBM. This supports higher power budgets and reliability in servers under air-cooling conditions.

{kind=link}

The broader trend I’ve noticed in the industry is a gradual shift toward hybrid bonding (direct Copper-to-Copper and dielectric bonding, DBI for short) for advanced packaging in HBM, chiplets, and 3D integration (HBM-on-GPU). It replaces or augments traditional thermo-compression bonding (TCB) / micro-bumps for finer pitches, better thermal & electrical performance, and thinner stacks. Major players like Samsung, SK hynix, TSMC, Intel, and Micron, are advancing this. In my opinion a the true winner agnostic beneficiaries of this are companies that provide equipment, metrology, IP, testing, and specialty manufacturing.

I’ve owned and continue to own $ONTO, $COHU, and $RMBS, specifically to get exposure to the Hybrid Bonding supply chain. All these stocks have more than doubled for me and I believe this theme/narrative is just starting to develop. There is another angle that seems very attractive to me right now. I'll talk about the stock and my thesis behind it in Part 2 if people are interested.

u/Optimal_Image5192 — 11 days ago

▲ 37 r/sp500

$IBM Unveiled Research-Stage Sub-1nm Chip Technology 👀

$IBM just unveiled research-stage sub-1nm chip technology using a 0.7nm “nanostack” 3D transistor design.

The company says it could pack nearly 100 billion transistors on a chip the size of a fingernail — delivering up to 50% more performance or 70% better efficiency vs. its 2nm node.

u/Optimal_Image5192 — 11 days ago

▲ 105 r/StockMarket

Are Solar Names Setting Up for a Big Move? I Think Yes… (Part 2)

I wrote part 1 of my thesis on solar as a sector on another subreddit, but I don’t think people were interested in reading the research as much there :(. I broke down the trend we’re seeing with additional utility-scale generating solar capacity being brought on by U.S. developers and power-plant owners, how solar had one of the largest power generation requests based on Texas ERCOT’s February 2026 generator-interconnection queue, how California has already shown the possibility with solar and much more. If you’re interested in the detailed research you can find it on my page easily or not (totally up to you).

In this post I wanted to share with you guys (cause I think people actually appreciate reading and understanding the research here more) which solar names I’m interested in and why.

Potential Good Risk-to-Reward Exposures (In My Opinion)

One thing to note about the case I’m making here is that I’m not claiming “Solar will power data centers.” My claim is specifically, “Data center load growth is forcing the U.S. power grid to add capacity quickly, and solar + battery storage should capture a significant share of that incremental capacity.” With this distinction made, we can determine the supply chain:

- Utility-scale solar

- Battery storage

- Electrical balance of systems

- Grid interconnection

- Domestic manufacturing

- Power electronics

- Transformers, switchgear, cabling, and substation infrastructure

- Behind-the-meter and near-site power systems for hyperscalers

Last year my best picks in this supply chain were battery storage players. I bought $ENS at ~$120/sh and $AMPX at ~$9/sh. Both those plays have done quite well and I still continue to like both of them, but in terms of solar specific names the two names I like are, $SHLS and $TE. Let’s talk about why…

Shoals Technologies

Shoals Technologies is not just a solar-panel story. They sell Electrical Balance of System (EBOS) infrastructure. This includes the components that move current from solar panels to inverters and ultimately to the grid. Shoals describes EBOS as mission-critical infrastructure, including cable assemblies, fuses, combiners, disconnects, recombiners, wireless monitoring, junction boxes, and their plug-and-play system architecture.

In the last quarter (Q1 2026), they reported almost 75% revenue growth YoY, $140.6 million, from $80.4 million. Adjusted EBITDA rose to $21.1 million, and backlog plus awarded orders reached a record $758 million, up 17.5% YoY. Management guided Q2 revenue to $150–170 million and raised full year 2026 guidance to $600–640 million of revenue and $118–132 million of adjusted EBITDA. This imo is the cleanest evidence of my original thesis and I think a really good exposure. It shows, in my view, that solar and a solar company can grow even through the political noise.

Their data center angle is what’s attractive to me. Shoals says their solutions support utility-scale solar, battery storage, and data-center power systems, and they market their prefabricated plug-and-play architecture as useful for mission-critical infrastructure. The reason this matters is that data-centers are becoming more like utilities when it comes to power in my view. They need large electrical yards, battery systems, high-current DC architecture, rapid deployment timelines, and extreme reliability requirements. EBOS, I believe, is directly relevant wherever large solar and storage systems are being built to support data center load.

Their current enterprise value is ~$1.85B, and the stock trades roughly at 3x sales, ~15x forward EBITDA, ~19x trailing EBITDA and with ~$170M in debt. Using peers as benchmark, $NXT trades at ~28x, $APH trades at ~27x, and $ARRY trades at ~18x, trailing EV/EBITDA. With the specialized niche they offer with EBOS and the 50-70% guided revenue growth, backlog converts, stabalizing tariffs, and margin recovery, $SHLS looks like a good risk-to-reward play for me to express my solar thesis.

The main risks in my opinion are: gross margin pressure, tariffs, legal/warranty overhangs, project timing, competition, customer concentration, and whether data center demand translates into actual orders rather than just broader sector demand.

T1 Energy

T1 Energy is a different and very interesting kind of bet, in my opinion. This is a crowd favorite name, recently Leupold disclosed his stake in it too. T1 is trying to build an integrated U.S. solar and battery supply chain. They operate the G1 Dallas solar-module facility and is pursuing vertical integration, including domestic solar-cell manufacturing.

In Q1 2026, they reported $177.6 million of net sales, up from $53.5 million in the prior year period. Management maintained 2026 G1 Dallas production guidance of 3.1–4.2 GW and said customer demand for G1 and G2 production in 2027–2028 covered more than 100% of their planned capacity.

The G2 Austin cell facility is the strategic asset for them in my view. They’ve said that Phase 1 is designed for 2.1 GW of solar cell production, with initial cell production targeted for Q4 2026. If successful, I think it would reduce reliance on imported cells, improve domestic positioning, and potentially make T1 more valuable under U.S. supply chain and tariff regime.

They announced acquisition of KORE Power which I think gives them exposure to data centers and battery storage. They’ve said that KORE gives them an entry point into BESS integration, software, and a renewables & infrastructure division that has supported more than 1,100 BESS projects globally. They expect the acquisition to contribute $15–20 million of EBITDA in 2027, assuming the deal closes and performs as expected. This is a plausible pivot that makes them interesting to me. Solar modules alone are more commoditized, but solar + domestic cells + energy storage integration + data center infrastructure says a much better story in my opinion.

But there are risks here. T1 energy is capital intensive, manufacturing execution is not the easiest of tasks, and the balance sheet is a bit complicated. As of Q1 2026, T1 reported $123.7 million of cash, cash equivalents, restricted cash, and restricted cash equivalents, but only $46.4 million of that was unrestricted cash. They also had meaningful debt and liabilities in my opinion.

So $TE is not a simple “solar is undervalued” story. I view them closer to an industrial policy/manufacturing ramp with meaningful operating leverage. If G1 ramps, G2 qualifies, customers convert, and KORE gives credible storage exposure, the upside can be meaningful, in my opinion. The risks here are finances tightening, policy shifts further against domestic credit monetization, and/or manufacturing margins disappoint. This, in my view, is definitely a higher-beta and more speculative story than $SHLS, but for me I like the risk-to-reward.

With that I thank you for reading my thoughts and opinions. I’m typically a micro-economic guy, meaning I post about individual stocks and sectors that I think are interesting. I tend to do a lot of research (more than what I posted here) and build my conviction. I hope this research helps you understand these industries better, and gives you an insight on how I look at equities/investments.

Please remember that I can be wrong and make mistakes. I am a human, I do often miss key facts and once they are know I will change my views. Please do not use this as financial advice. This is NOT FINANCIAL ADVICE! I’m just some guy on the internet who likes to research companies and industries. You should use what I write here as educational or entertainment, nothing else. I’m not a financial advisor. Do your own research before making any investments.

u/Optimal_Image5192 — 11 days ago

▲ 7 r/sp500

Amazing Top and Bottom Line Beat on $MU

$MU Revenue: $41.46B (Est. $35.5B)

Adjusted EPS: $25.11 (Est. $20.4)

Adjusted Gross Margin: 84.9% (Est. 81.8%)

Adjusted Net Income: $28.86B

Adjusted Operating Income: $33.68B

Adjusted OpEx: $1.52B

Investments in CapEx, net: $7.1B

Cash, marketable investments, and restricted cash: $30.2B

Q4 Guidance looks fantastic imo:

Revenue: $50.0B ± $1.0B (Est. $43.4B)

Adjusted EPS: $31.00 ± $1.00 (Est. $24.3)

Gross Margin: Approximately 86% (Est. 83%)

OpEx: Approximately $1.65B

Operating Cash Flow: $25.39B

Adjusted FCF: $18.3B

Commentary from CEO, “Micron’s record fiscal Q3 financial results and even stronger outlook for Q4 reflect the strategic value of memory in the AI era.”

HBM4: In high-volume shipments for lead customer platform; qualification samples shipped to multiple end-customers

HBM4E: Volume production expected in calendar 2027

G9-based PCIe Gen6 high-performance SSD: In high-volume production

High-capacity 245TB QLC SSD: Shipments commenced

Based on this, it makes $MU the top 5 company based on revenue lol.

u/Optimal_Image5192 — 11 days ago

Nokia is Deepening Its Autonomous Networks Strategy by Partnership with Amazon’s AWS and Databricks.

Nokia ($NOK) is advancing autonomous networks by running its Autonomous Network Fabric on AWS. This will give telecom operators access to advanced AI and cloud-based tools designed to reach Level 4 network autonomy, with availability targeted for later in 2026.

The platform brings together intent-based service orchestration, AI-driven anomaly detection, root cause analysis, automated closed-loop resolution, digital twins, and agentic AI capabilities.

Separately, Nokia has completed a PoC with Databricks to create a unified, cloud-agnostic telecom data platform. The goal is to channel real-time network data directly into AI agents for faster, automated decision-making across different network domains.

Nokia notes that its existing autonomous networks portfolio has already delivered strong results for operators, including automation rates above 90% and up to an 85% reduction in the time required to roll out network slices.

u/Optimal_Image5192 — 12 days ago

$FIVN (Five9) Launches Breakthrough New Release of Voice AI Agents to Power Next-Gen Agentic Self-Service

I wrote a lengthy article on why I think select software names might be unreasonably getting sold off due to AI related pricing power headwinds. In that article I wrote my thesis on $FIVN (there are more names I like in this space as well, just haven’t had a chance to condense my research in a publishable format yet :/) and why I think there is a big opportunity for earnings growth and gross margin expansion.

This morning at Customer Contact Week / CCW in Las Vegas, Five9 announced a major new release of their Voice AI Agents, positioned as the next evolution of agentic self-service. It runs on a brand new, purpose-built architecture designed specifically for the “agentic era,” moving far beyond traditional scripted bots and legacy Interactive Voice Response (IVR) systems.

These agents are built to reason, take real actions, and solve complex customer requests while enabling smooth, contextual handoffs to human agents when needed.

Their new research shows that 65% of organizations are now implementing/releasing at least one AI use case in CX. Self-service automation is a top priority (42%).

Early rollout exceeded containment targets, reduced handle times, and delivered more consistent human-like interactions. One of their customers, PODS, expects the agents to handle over 100,000 service calls by end of the year.

Analyst Maribel Lopez (from Lopez Research) highlights the industry shift from basic AI responders to true agentic systems that complete tasks, plus the critical need for governance and controls at scale.

Main Features & Capabilities of the New Agentic Platform

Human-like voice interactions: Low-latency streaming, natural turn-taking, interruption detection, multilingual support, and strong background noise handling.

Action-oriented AI (not just chat): Secure tool-calling to connect with enterprise systems. For example, authenticating customers, updating records, processing transactions, or completing tasks in real-time.

Seamless AI + Human collaboration: Full conversation context transfers instantly when the call is being transferred from an agent to human using Five9’s platform.

Enterprise-grade governance & trust: Built-in guardrails, automated post-call AI evaluations, LLM blinding (to protect sensitive data), and workflow verification.

New AI Agent Studio: Unified environment for building, testing, deploying, monitoring, and improving agents (includes call testing, versioning, rollbacks, and post-call analytics).

Platform advantage: Powered by the proprietary Agentic Voice Switch architecture, natively integrated into Five9’s carrier-grade telephony platform (no BS add-ons). Data, knowledge, and orchestration are shared across the full Intelligent CX Platform.

This is the quote from CEO Ajay Awatramani:

“Five9’s new Voice AI Agents represent a breakthrough in AI, delivering natural, human-like interactions with exceptional responsiveness, accuracy, and scale, seamlessly orchestrated with human agents on the Five9 Intelligent CX Platform.”

Conclusion

This, in my opinion, is a significant product announcement from them directly my thesis around production and deployment of agentic AI for voice self-service, with strong emphasis on real actions, human collaboration, and scalability.

People often think of Five9 as another chatbot customer service provider, but this goes against that narrative imo. In my view the market is severely mispricing their platform and the need for AI voice agents in customer service.

As always I can be wrong, I don’t have a crystal ball, but I’m at least putting my money where my mouth is lol. None of this is meant to be financial advice! I’m just a guy on the internet sharing my thoughts and opinions on the market.

u/Optimal_Image5192 — 12 days ago

▲ 1 r/Stocks_Picks

Are Solar Names Setting Up for a Big Move? I Think Yes... (Part 1)

During my undergrad years, I remember Photovoltaics (PVs) and solar were the talk of the town. I recall almost all of my professors and their students were working on designing solar cells that would yield high power conversion efficiency at low costs. That was how I was introduced to the world of semiconductors (back in 2018 lol). I worked quite a bit on Perovskite solar cells (unimportant to this discussion) as an undergrad and my first year as a PhD. I knew the capabilities AND limitations of solar back then and always thought of them as interesting, but limiting without Battery Storage Systems (BESS). So why am I sharing this now? “Who cares if you did your silly little solar project?”

Well based on recent trends seen in the U.S. power grid build out and the increase in demand for more data-center related power capacity, I think solar is setup for a significant re-rating.

The policy overhang is real

Over the past year and a half (since the election) there has been a significant overhang on Solar companies. The Trump administration has not been shy in showing their bias toward solar. The White House has explicitly framed wind and solar subsidies as market-distorting and directed several U.S. agencies to restrict support for solar credits where possible. The July 2025 executive order specifically called for enforcing the repeal or modification of wind and solar tax credits under the One Big Beautiful Bill Act.

The tax-credit regime has also become more hostile. The IRS Notice in 2025 restricted the use of the previously allowed 5% spending safe harbor, forcing larger projects (like wind and most solar >1.5 MW) to rely solely on the physical work test along with the foreign entity restrictions penalizing prohibited foreign entity (PFE) and Foreign Entity of Concern (FEOC) projects for receiving material assistance from restricted entities. Solar Energy Industries Association (SEIA) says that to qualify for the 48E and 45Y credits, many solar projects must either begin construction by July 4, 2026 or be placed in service by December 31, 2027, with additional FEOC restrictions beginning in 2026. Treasury and IRS also issued guidance on PFE restrictions affecting 45Y, 48E, and 45X credits.

Residential solar is under even more direct pressure in my opinion. The IRS said the Residential Clean Energy Credit (RCEC) is not available for expenditures after December 31, 2025.

These are all the policy and political overhangs that, in my opinion, have suppressed valuations for lot of these solar companies. I believe they are trading with a “political risk” discount, and for a legitimate reason. The tax-credit uncertainty, FEOC compliance, tariff exposure, DOE hostility, permitting friction, all in my opinion fuel investor fear that the sector’s fundamentals are politically fragile. However, in the midst of all this bearish sentiment, the one thing that, in my opinion, is not being priced in is that the power grid data is not cooperating.

Capacity Additions Could Overwhelm the Political Narrative

The most important data point for me is national. The U.S. Energy Information Administration (EIA) expects U.S. developers and power-plant owners to add 86 GW of new utility-scale generating capacity in 2026. This would be the largest annual addition in EIA’s dataset so far. What’s more interesting is that solar is expected to be 51% of those planned additions, with batteries at 28% and wind at 14%. Developers plan to add 43.4 GW of utility-scale solar in 2026, up 60% from 2025. Texas alone accounts for about 40% of planned new solar additions, and Texas is no liberal state, at least in 2026 lol.

{kind=link}

This is the core of the bull/value case I’m trying to make; even under immense political pressure, there is increasing demand for additional solar capacity for the U.S. power grid.

SEIA and Wood Mackenzie’s Q1 2026 data strengthens the point. The U.S. installed 7.8 GW of solar capacity in the first quarter, and solar plus storage represented 91% of new electric generation capacity installed during the quarter. Their report also says that contracts for utility-scale solar increased 15% YoY, driven largely by, you guessed it, power demand for AI hyperscalers and data-centers. Notably, states that voted for Trump in 2024 accounted for 74% of solar capacity installed in Q1 of 2026.

That last point is important because it shows that solar adoption is no longer just a California or a liberal state climate based policy push. It is now pushed by power, interconnection, and time-to-capacity demand for AI advancement. Texas, Arizona, Florida, Ohio, Indiana, Michigan, and Mississippi are not building solar because they are trying to signal progressive energy politics. They are building it because, in my opinion, solar is fast, modular, cost-effective (this is debatable), and increasingly paired with batteries.

This is where, in my view, the political narrative and the bear case starts to break down. The federal government can get rid of the incentives for the sector, but grid operators, utilities, developers, and hyperscalers still need to bring on capacity. In fact, solar companies may no longer need those incentives or favorable policy narratives to show growth. There might be/already is a demand for them.

ERCOT is the Clearest Evidence

Texas is the most important case study because it breaks the notion that growth in solar companies is merely a blue-state subsidy artifact. As of Electric Reliability Council of Texas’s (ERCOT’s) February 2026 generator-interconnection queue, the system had about 453.6 GW of active generation requests. The largest categories were: Energy storage with 177.6 GW, Solar with 162.9 GW, Natural gas with 60.7 GW, and Wind with 47.8 GW. This shows that solar and energy storage represented more than 76% of power generation seeking interconnection.

EIA also expects solar power generation in ERCOT to surpass coal for the first time in history, in 2026, with solar producing about 78 billion kWh versus coal at about 60 billion kWh. From 2021 to 2025, solar generation in ERCOT rose from 4% to 12%, while coal fell from 19% to 13%. EIA explicitly ties rising ERCOT demand to data centers, crypto mining, industrial electrification, and oil & gas sector growth.

Data source: U.S. Energy Information Administration, Short-Term Energy Outlook, Table 7d

{kind=link}

This, in my opinion, is the bull case for the sector. Data-center load is quickly growing in Texas, and the resources trying to interconnect are dominantly solar and storage.

The Potential Midterm Elections Tailwind

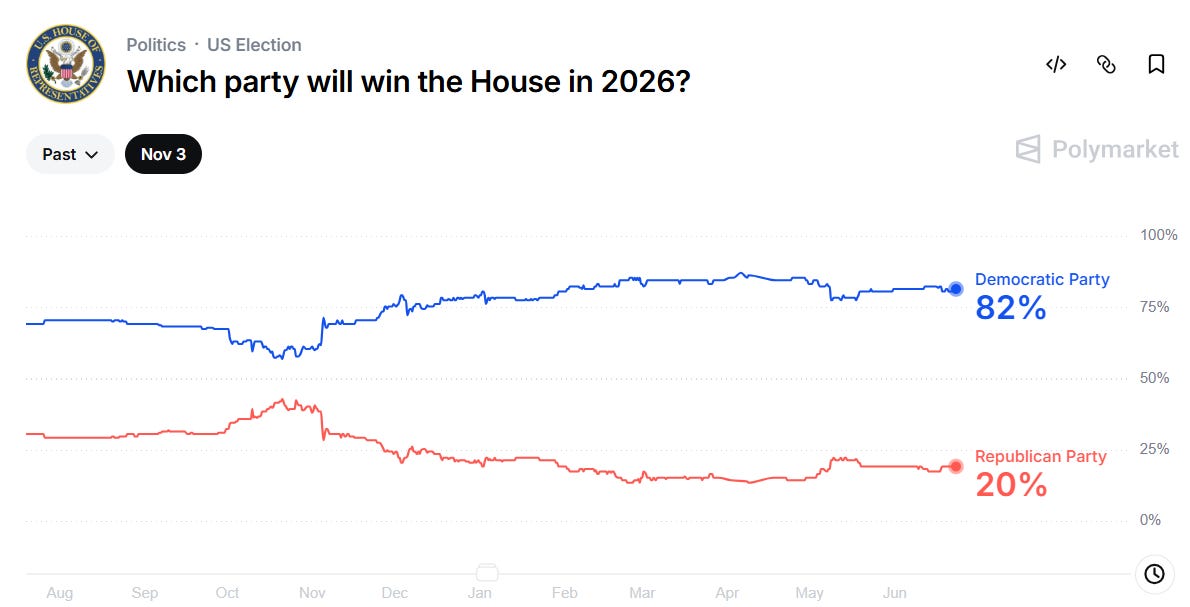

{kind=link}

{kind=link}

Recent prediction markets trends have supported a “blue-wave” during the midterm elections of 2026. A Democratic midterm win, or even a narrower Republican majority, could relieve some policy pressure on solar names in my opinion. The market would likely reprice the probability of further tax-credit erosion, harsher FEOC enforcement, anti-solar executive actions, or DOE funding hostility.

But I would not make that the primary thesis.

The stronger argument, in my view, is that solar is working despite a hostility from Trump administration. If the political backdrop improves, that is upside is an optionality. The base case, however, still rests on the power grid demand for me.

Prediction markets can move sentiment, but they are not a substitute for capacity data, backlog, interconnection queues, or earnings revisions.

Data Centers Turn Solar from a Climate Trade into a AI-Power Infrastructure Trade

The traditional narrative with solar companies has mostly been about decarbonization, subsidies, ESG, and residential adoption. Remember those Tesla Ads about solar roofs… That narrative got hit hard by higher rates, net metering changes, policy risks, and weak residential adoption. Don’t believe me, pull up a chart for most popular solar names, $RUN, $ENPH, $FSLR, $SEDG, $ARRY, etc. Notice where they’re trading relative to their all-time-highs.

I believe there’s a new narrative in town…

U.S. DOE (Department of Energy) and Lawrence Berkeley National Labs estimate that data centers in U.S. consumed roughly 176 TWh in 2023, which is ~4.4% of total U.S. electricity consumption. They project data center consumption could reach 325–580 TWh by 2028, roughly 6.7–12% of total U.S. electricity consumption. EPRI’s 2026 analysis is even more aggressive. They project data centers could consume 9–17% of U.S. electricity by 2030, up from 4–5% today.

That scale, in my opinion, changes the narrative. The issue is no longer whether policymakers like solar. The issue is whether the grid can add enough capacity fast enough. Solar and batteries are not perfect, but they are available, modular, and deployable right now. That is why solar keeps showing up in the capacity addition data in my opinion. So the new narrative for solar, in my view, is “The U.S. needs a massive amount of new electricity capacity, and solar is one of the few technologies that can be deployed quickly enough to matter.”

So now that we know the reasoning behind the speculation and why solar companies have potential to re-rate, where do I see the opportunity? That's saved for PART 2...

u/Optimal_Image5192 — 12 days ago

▲ 85 r/sp500

South Korea’s 🇰🇷 KOSPI Index Fell 10%, Second Worst Session Since 2008.

The entire reason KOSPI was down 10% yesterday, marking it the third biggest one day drop ever, was due to memory news from SK Hynix. SK Hynix is deliberately slowing their HBM4 production ramp by delaying conversion of some HBM3E lines to focus resources on commodity DRAM, which delivers higher operating margins than HBM due to supply shortages.

The strategy is to use their established 40%+ HBM revenue lead and strong position through 2026, while commodity DRAM ASPs have risen sharply and margins could potentially reach 90%, with analysts raising earnings forecasts on broader memory pricing strength.

SK Hynix and Samsung (making up ~54% of the index) got hit hard. $SPY, because of the $MU and overall AI supply chain, has become a lower-beta proxy to KOSPI at this point, which is why you’re seeing a selloff in premarket imo.

Not Financial Advice! Just sharing my thoughts/opinions on why I think we’re seeing a selloff.

u/Optimal_Image5192 — 13 days ago

▲ 408 r/sp500

BofA Expecting 3 Rate Hikes in 2026…

BofA now expects the Fed to hike rates 3 times this year, shifting from its prior view of no changes.

BofA sees 25 bps hikes in September, October and December, taking rates to 4.25%-4.5% by year-end.

And expects the Fed’s first rate cuts to come in 2028.

u/Optimal_Image5192 — 14 days ago

▲ 3 r/sp500

The Warsh Era Begins: A Hawkish Pivot, the End of Forward Guidance, and Implications for Inflation and Equities

Today on June 17, 2026, the new Federal Reserve Chair Kevin Warsh successfully (questionable) completed his first FOMC meeting and delivered a press conference that clearly pivots from the communication style that the markets have been used to from his predecessor, Jerome Powell (never forget 🫡). The good news for the market is that the Committee decided to hold the federal funds rate steady at 3.50–3.75 percent in a unanimous 12–0 vote. While this decision was mostly baked into the market and pretty much expected by most traders, Warsh’s tone, policy signals, and structural announcements, in my view, sent a hawkish message that I think might’ve spooked the markets.

I’ll attempt to break down what Warsh said, the context of the questions he faced, the shift in the inflation narrative, and give my thought on what this means for the equity market, including the S&P 500 ($SPY). So let’s dig in…

The FOMC Decision and Economic Backdrop

The official FOMC statement, in my view, painted a resilient but challenged economy narrative.

*“Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little. Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee will deliver price stability.”*

Now let’s address the elephant in the room: This statement is incredibly short, and it’s almost completely stripped of any insightful forward-looking statement. This is a very different communication style than what we’ve been used to. In my view, this alone is not a huge issue. I’m willing to give a lot of leeway considering this is his first meeting, and Warsh has been known to be keeping things short, sweet and to the point. So he has to establish his role and methods.

Now here’s the part that started to worry me a bit. Still too early to tell, but a note has been made in my noggin. The Summary of Economic Projections (SEP) reinforced a more cautious outlook. Inflation forecasts were revised higher (with 2026 PCE inflation now seen around 3.6 percent in some reports), GDP growth projections were trimmed (to roughly 2.2 percent), and the dot plot showed a hawkish tilt: a higher median path for rates by year-end, **with several participants seeing the possibility of rate hikes rather than cuts.**

Warsh’s Stance: Hawkish, but Not Recklessly Hawkish

In my view one of the most important line from the FOMC is his inflation credibility frame: **“This committee will deliver price stability.”** He tied that to inflation having run above target for more than five years (little jab at my man Powell :/) and said high prices remain a burden. That, in my opinion, is the central message of the meeting.

*“The commitment to deliver is strong, unanimous, and unambiguous, and that’s I think an important message we’ve missed for five years, and we’re going to fix that.”*

I interpret that as him criticizing Powell’s leadership allowing inflation to remain above target for too long following the post-COVID surge. Warsh pushes on this narrative further by stating that “inflation is a choice” and that the Committee would deliver on price stability.

He also kept the 2% target intact. When asked whether the inflation framework review includes reconsidering 2%, he said:

*“I see no reason, until we have reestablished our commitment and ability to deliver on the 2% inflation objective, to revisit that.”*

That matters because in my view this rules out the dovish escape hatch of raising the target to 3% or redefining success. To be fair he didn’t say “we are hiking next meeting.” He held the target range at **3.5%–3.75%** and said the committee maintained ample reserves. The median SEP had the fed funds rate at **3.8% at year-end** and **3.6% next year**, while total PCE inflation was projected at **3.6% this year**and **2.3% next year**. This is a clear sign in my eyes that policy is restrictive enough for now, but with a clear hiking bias if inflation does not remain in-line with their targets.

When asked how restrictive the policy is, he said it’s **“uneven”**. Housing looks “somewhat restrictive,” but he would have a “hard time” saying that when looking at financial markets. That is an important market signal: in my opinion, he is effectively saying financial conditions are not doing enough tightening.

The Good Ol’ Task Forces…

He announced the creation of five independent task forces to review core aspects of monetary policy operations:

• Fed communications

• The Fed’s balance sheet

• Use and reliance on existing data sources

• Productivity and jobs

• The Fed’s inflation frameworks

Their mandate is to “start with first principles, ask hard questions, examine current practice, consider alternatives, and ultimately propose next steps.” He expects them to begin within weeks, provide framing by fall, and mostly conclude by year-end. He isn’t just reviewing inflation strategy; he is reviewing the communications apparatus, the balance-sheet regime, official data reliance, AI/productivity effects, and inflation measurement/frameworks.

I think what matters (or should matter) the most to the market is the communication task force. He explicitly said it may propose changes to the SEP, and later said the review could include “press conferences, dots, meetings and the like, transcripts, minutes.” This is where I start getting concerned.

Warsh explicitly stated that the Fed would no longer provide the detailed forward guidance markets had gotten used to under J Powell. He noted that **“so called forward guidance was not well suited to the current policy conjuncture”** and that the Committee had agreed to drop it. When pressed for signals on the next moves, he replied along the lines of: **“I can’t give you any guidance on what we’re going to do next.”** This I very much don’t like >:(. I think going forward this is going to create more volatility in the markets around FOMC and who likes less transparency? Warsh, clearly.

*Side note: I think the market should also care about the balance sheet task force. It will review the benefits and risks of the ample reserves regime and the composition of the balance sheet. This, in my view, raises the possibility of a different liquidity regime over time. I would not price an imminent QT shock from this alone, because he reaffirmed ample reserves for now, but the direction of travel is toward asking whether the post-GFC/post-COVID operating framework is still appropriate ?*

Transparency Should Matter…

As a market participant, my job is to speculate. Speculate on an asset class, or equities or industries/sectors, etc. I’m always thinking about the potential of an asset in the future adjusted for current risks, and making a decision to trade it. What makes my speculation better, and it’s also the reason why I think America is the greatest country in the world with the greatest stock market in the world, is transparency. Understanding that public companies and even the federal government has to publish data for me to review, allows me to make informed speculations. As a speculator in the market, it’s concerning to me that we will no longer have forward guidance from the fed.

Warsh said the statement was shorter, simpler, and that

*“Absent also is so-called forward guidance, which we agreed was not well-suited to the current policy conjuncture.”*

He also personally refused to submit SEP projections because, in his words, “For me, it’s not helpful in the conduct of policy.” In my view, this was him signaling to the market that he does not want to disclose what is coming next:

*“I can’t delve you any forward guidance about what we’re going to do next.”*

Avoiding Important Questions

He downplayed the dot plot in the Q&A section. When asked about nine members suggesting a rate increase by year-end, he said the submissions came with “pencils, those kind with the big erasers” and said he heard “not tons of conviction.” Bruh, what?? In my view, this reduces the informational value of the dots. Markets, in my opinion, can no longer treat the median dot as quasi-guidance if the chair is openly telling you the dots are provisional and not central to his own policy process 😂

This wasn’t just one evasive answer. He avoided specific reaction function questions several times. What would trigger hikes, whether press conferences will continue after every meeting, market reaction, and his own reaction function. In one case he said, “I’ve got nothing more to say than the statement itself.” In another, he called his reaction function answer “very unsatisfactory.”

This is all, in my opinion, is less transparent, even if Warsh paints it as cleaner and more efficient. And to certain extent I don’t fully disagree with him either, but as a market participant what I see is that the fed will say less about the path and more about the objective. That increases the value of data releases and potentially increases uncertainty around each FOMC meeting. And I’m just grumpy about it :/.

Playing Devil’s Advocate

His argument is coherent in my view. Markets can become less useful if they simply mirror the Fed’s guidance back to the Fed. He said financial markets work best when they react to incoming data, and worse when they focus on “how will the Federal Reserve react to that incoming information.” He added that market prices are an important input for central bankers, but if prices merely reflect Fed guidance, the Fed is “being blind” to one of its most important information sources. This is not a bad argument at all. In fact, it’s a real critique of the Powell-era communication loop where Fed guides markets, markets price the guidance, Fed reads market pricing as information, and policy becomes endogenous to its own signaling. Warsh simply wants to break that loop.

The problem for risk assets is that in my opinion this means the Fed put becomes less legible. The market no longer gets as much advance notice of policy pivots. That tends to raise rate volatility, equity volatility, and the equity risk premium.

What Does This Mean for S&P 500?

As I laid out my case, and my qualms with this “less-transparency” approach solely as a market participant, I think for $SPY, the conference is not bullish on first read, as we saw by the -1.5% reaction post-FOMC meeting. The policy mix as I see it: no cut discussion, inflation credibility prioritized, rate hikes not ruled out, less forward guidance, and a chair who says financial markets do not look very restrictive. That to me is a multiple compression language.

The key quote for equities is not just “deliver price stability.” It is this: “I would have a hard time” saying policy is restrictive when looking at financial markets. That sounds like a Fed chair who is not alarmed by elevated equity prices and may not rush to cushion a drawdown unless it threatens the macro outlook. So the bull case for $SPY now needs earnings/productivity to carry more weight, because policy signaling going forward, in my view, will be less supportive. The market can still rally if inflation cools and AI/productivity keeps nominal growth strong, but the path, in my opinion, will be potentially more volatile because the Fed is no longer spoon-feeding the expected rate path.

Conclusion and My Final Thoughts.

I think today’s conference was a “controlled hawkish reset”. Warsh, in my opinion, is trying to rebuild inflation credibility without shocking markets with an immediate rate hike. But he is also intentionally removing some of the market’s comfort blanket.

This is **NOT** me being bearish or calling for a crash. He did not hike rates, he did not abandon the 2% inflation target, he did not announce balance-sheet tightening, and he acknowledged stable labor markets and productivity strength. But as a speculator, I would treat this as another risk factor you have to account for to have exposure to the market (specially for someone like me who runs a very high beta portfolio).

For $SPY specifically: I think there might be some volatility, but I don’t have a crystal ball that allows me to predict the future. The conference, in my opinion, adds higher realized volatility, more sensitivity to CPI/PCE/payrolls, and a little tougher environment for long-duration growth multiples unless yields stabilize. What would make me feel very secure and “really hit the gas”, proverbially speaking, is if either the inflation data softens fast or Warsh clarifies that communications reform does not mean materially less information. But again I take macro signals with a grain of salt. There are so many variables that change so quickly that it’s almost pointless, at least to my process and the type of investing I do, to put too much emphasis on one macro data point. What matters to that market today, tomorrow may even be forgotten.

Thank you for listening to my very long rant. I’m typically a micro-economic guy, meaning I post about individual stocks and sectors that I think are interesting. But this seemed important to me and so of my stock considerations, so I wanted to share my thoughts and opinions with you all.

*Please remember that I can be wrong and make mistakes. I am a human, I do often miss key facts and once they are know I will change my views. Please do not use this as financial advice. This is NOT FINANCIAL ADVICE! I’m just some guy on the internet who likes to research companies and industries. You should use what I write here as educational or entertainment, nothing else. I’m not a financial advisor. Do your own research before making any investments.*

u/Optimal_Image5192 — 18 days ago

▲ 1 r/Stocks_Picks

AI Will Kill All Software Companies… Or So the Crowd Believes.

Over the past 3 years we’ve seen a huge surge in AI related equities. Markets have absolutely rewarded anything that touches this trade ever since we had the ChatGPT moment back in 2023 (the good old days). One sector that has taken a significant hit recently is $IGV (software).

Lot of investors look at software stocks and see “dead money.” In fact many of my friends whose opinions I value have been talking about never touching software names with “a 20 ft pole”, whatever that means… Valuations have come down significantly for a lot of software names from the pandemic highs, growth shows signs of slowing, and the market is skeptical that AI will completely diminish the pricing power of these companies and margins will be crushed. I get it, plenty of flashy AI stories have disappointed.

But I’m a contrarian at heart. There’s a reason why my Reddit has negative karma lol. I always play devil’s advocate and try to understand the “why” of something before attaching myself to an idea. So why am I interested in software? And which software company is speaking to me right now?

When you call a company for help, whether it’s your bank, internet provider, or retailer, you’re usually talking to someone (or now, something) in a contact center. These are the modern versions of old-school call centers. Companies track everything here: how long calls take, whether the issue gets solved on the first try, how happy customers are, and how productive their staff is. It’s one of the clearest, most measurable places where AI can deliver quick, obvious wins for businesses.

AI is capable of dramatically cutting costs for businesses here. Companies using these tools often see handle times drop by 2 minutes per call, calls fully handled by AI rise significantly, and overall operational savings in the 20-60%+ range depending on the use case. This reduces operational costs by a significant amount especially for smaller businesses.

Margin expansion for your customers, in my opinion, is one of the best win-win scenarios that can drive pricing power for a lot of companies. “Hey I know you’re spending hundreds of Billions on something you don’t really care about, but kinda sort need. I can offer you a solution that’s potentially better and 100x cheaper. Just pay me a little premium.” YES. PLEASE.

In my opinion, $FIVN is a great exposure here. Five9, in my opinion, is a clear leader in cloud based contact center software (or CCaaS). Their Genius AI suite includes a bunch of tools like AI agents that handle routine customer conversations (and smoothly hand off to a human when needed), AI that transcribes and summarizes calls, spots insights, helps agents in real-time, automates workflows, and more. It’s designed to make customer support faster, MUCH cheaper, and better.

What makes them more compelling is the fact that they own the underlying voice infrastructure that makes realtime Voice AI actually function properly. Their Global Voice network delivers low-latency calls worldwide with strong reliability and backup carriers. They also have VoiceStream, which lets audio and call data flow in real time to AI systems for things like sentiment analysis, coaching, or biometrics.

So they sell their own AI tools directly AND also help power other companies’ voice AI products. Forrester’s study of Five9 customers showed a 212% ROI and $14.5 million in net value over three years. These savings create strong customer demand: companies see clear margin improvements from lower support costs, so they’re eager to adopt and expand. That gives Five9 pricing power and stickier relationships as clients migrate from outdated on-premise systems.

On top of that, customer service hiring is growing faster than the overall job market right now. That means more demand for efficient tools to handle the workload without endlessly adding headcount.

The stock looks very attractive to me here on valuation basis with ~1.2x sales, ~6x free cash flow, 55% gross margins, almost no debt, and plenty of cash on hand. That’s cheap for a company with this kind of growth runway in my opinion.

Their latest earnings showed that AI revenue jumped 68% YoY (40% sequentially from prior quarter), now running at over $125 million annually and making up 13% of subscription revenue (up from 8% YoY). That’s tells me there’s a real inflection point here.

In short, my thesis here is that when AI handles more calls and reduces the need for human agents, the dollars don’t leave the contact center, they just shift from labor to software. Enterprises spend massively on customer support staff. Five9 sees the total opportunity as a $24 billion cloud software market plus a huge $210 billion labor arbitrage play through AI. In other words, companies won’t cut their support budgets; they’ll reallocate money to smarter tools like Five9’s platform. This, in my opinion, expands their total addressable market significantly, and the stock price at these valuations is, in my opinion, not reflecting it.

If you’re interested in more detailed breakdown you can checkout my Substack article here, where I go over some numbers and more in-depth of why I think this theme is interesting.

This is NOT FINANCIAL ADVICE! I’m just some guy on the internet who likes to research companies and industries. You should use what I write here as educational or entertainment, nothing else. I’m not a financial advisor.

u/Optimal_Image5192 — 19 days ago

▲ 3 r/Stocks_Picks

$OUST Partners with Benchmark Electronics to Increase Production Capacity for Rev8 OS LiDAR Sensor Family 👀

$OUST partnered with Benchmark Electronics ($BHE) to scale manufacturing of the Rev8 OS lidar sensor family. Designed for mass-market adoption in automotive, robotics, and industrial applications, the highly automated production lines are built to produce over 100,000 units annually with a planned 10-year lifespan.

The Rev8 lineup introduces several hardware upgrades powered by Ouster's L4 and L4 Max silicon:

- Native Spatial Color: Fuses 3D depth data with 48-bit point-for-point color information. This allows the sensors to detect details like road signs and break lights without needing secondary texturing workflows.

- Improved Range & Resolution: Delivers up to double the range and resolution of the previous Rev7 generation, with the flagship OS1 Max offering up to 256 channels and a maximum range of 500 meters.

- Industrial and Automotive Grade: Features automotive-grade hardware, cyber-security, and functional safety targeting ASIL-B, SIL-2, and PLd certifications.

The sensors are fully integrated into major autonomy and edge-computing platforms, including the $NVDA Drive platform and Jetson ecosystem.

I’ve been long this name since mid $20s for robotics exposure and I can’t complain about their execution!

u/Optimal_Image5192 — 21 days ago

▲ 0 r/ValueInvesting

$SPCX Overvalued Argument is MISUNDERSTOOD and FLAWED!

Okay everyone seems to be hating hard on SpaceX, specially their valuation. Everywhere I go I find people commenting on ~$20B revenue with ~$2T market cap is crazy, etc, etc. I do agree that trading almost 100x TTM revenue is little cookie, but I think most people fail to understand the relative valuation case.

The bet with SpaceX ($SPCX) isn't what the company is doing today (the government contracts, xAI, Starlink, etc). It's about the potential TAM (Total Addressable Market). I'm not making a case for investing in $SPCX by any means. I have stayed away from the IPO and will not be touching it. My exposure to it was $IRDM which I bought end of last year at $17 and now it's at $50 something (not even tracking it anymore lol).

The goal of this post is to help you understand that the reason their valuations floats so high and why you can't compare them to $AMZN or $GOOGL or $META. That's like saying "Some AI stocks trade at 40-50x sales while some retail companies trade at only 2-7x sales. So AI stocks are bad." See that line of thinking inherently has a fallacy. Markets are a forward-looking mechanism. This means enough people collectively decided that they believe the opportunity (margins, TAM, growth, etc) going forward will be much different than represented in current valuations. It's all about speculation on the future, and if enough people believe it, the price action will reflect it.

So how does this tie into $SPCX?

Well now that you understand valuations aren't just numbers in the void, but always relative and indicative of a collective opinion of enough market participants, we can examine the space industry. What is the current TAM of the space industry? What rate is it expected to grow over the next year? 5 years? 10 years?? What are the opportunities and growth drivers that are/will be available to the industry as a whole? What are the risks? What would it mean if the industry as a whole succeeds at execution? Finally, am I and other market participants agree on the risk/reward on the industry?

Once you answer these questions, you will understand why the valuation for a leader and let's be honest, a monopoly as of now, is so high relative to their current annual sales. You may disagree with the execution, you may disagree with the market on the risk/reward assessment, you may even think that the potential TAM is exaggerated and on the timeline of growth. BUT you have to understand that you CANNOT claim $SPCX is overvalued by comparing it $AMZN or any other company that is not in the industry. That is a flawed argument imo.

I have MANY more thoughts on this, but I wanna open a discussion with this and see what people have to say. Would love any thoughts that people have. Agree? Disagree? Why? let's have a good, open discussion. I'm more than willing to talk and even change my mind if presented with good arguments.

u/Optimal_Image5192 — 21 days ago

▲ 7 r/ValueInvesting

$TKR - (The Timken Co.)

I first posted this thesis on my twitter when the stock was around \~114/sh. I think it’s a compelling opportunity for people looking to build robotics/physical AI exposure. I’ve copied and pasted that same thesis here if people are interested.

Actuators account for 40%-60% of the entire BOM for a humanoid robot. This is the single largest cost structure in the humanoid/robotics industry. Humanoids have not started scaling yet, but when/if they do, actuators will open up a huge market for hardware suppliers imo. The bet here is scaling of the TAM. Actuators for humanoids and most robots need electric motors and precision gearboxes, $TKR provides the latter.

Specialized and niche precision gearboxes (Harmonic Drives) are an integral part in humanoids' rotary joints—the shoulders, elbows, wrists, and hips—to allow movement. There is a huge shortage of supply for these Harmonic Drives, there's a tall ladder when trying to bring on additional supply capacity with high lead times in tools needed like Multi-axis CNC, High-Rigidity Precision Grinding Machines, material procurement takes 12-16 weeks, and quality assurance taking anywhere from 45 mins- 1 hour per unit. I'm personally betting that there will be a huge increase in demand for harmonic drives as the humanoid industry scales. Currently most of Harmonic drive suppliers are foreign (Harmonic Drive SE/Japan, Nabtesco/Japan) and private/smaller U.S. firms focus more on worm/planetary/slew but not strain-wave harmonic at scale. There is currently only one U.S. based supplier of Harmonic Drives, $TKR. Historically known as a heavy industrial bearing manufacturer, Timken has spent the last several years aggressively acquiring its way into the exact precision motion control niches causing this manufacturing bottleneck. Through its Industrial Motion segment, Timken owns the complete mechanical stack for robotics:

Cone Drive

$TKR acquired this European business in 2018. This is Timken’s direct asset for the bottleneck and why I'm interested in them. Cone Drive manufactures harmonic strain wave gearing (specifically targeting humanoid robotic joints like hips, knees, and wrists) out of U.S.-based manufacturing facilities. Acquiring them makes $TKR effectively the only U.S.-based public supplier of harmonic drives.

SPINEA (Acquired 2022)

Produces cycloidal reduction gears, which provide the high-load rigidity and torque needed for a robot's heavier structural axes (waist and shoulders).

CGI Inc. (Acquired 2024)

Specializes in high-precision, miniaturized gearheads and sub-assemblies historically utilized in surgical robotics and medical devices.

By rolling up Cone Drive, SPINEA, and CGI, Timken operates as a "one-stop shop" capable of supplying precision gear systems across all six axes of a robotic or humanoid actuator. What makes them even more interesting is that the high-growth robotics harmonic drive business is consolidated inside a massive legacy industrial business. Timken operates under two primary reportable segments:

Engineered Bearings (\~66% of FY '25 sales): This includes tapered roller bearings, spherical/ cylindrical roller bearings, ball bearings, and related components. Serves diverse end-markets including automotive, off-highway, rail, aerospace, wind energy, and general industrial. Revenue has been relatively stable/flat in recent years, with growth from pricing/mix and select markets (e.g., renewables) offset by softer demand in others. Q4 2025 sales +0.9% YoY; full-year adjusted EBITDA margin \~18.9–20.0%.

Industrial Motion (\~34% of FY '25 sales): This includes precision gearboxes and gears (via brands like Cone Drive, Spinea, and CGI), drives, breathers, seals, automatic lubrication systems, linear motion products, chain, belts, couplings, and industrial clutches and brakes. This segment has shown stronger growth: +8.4% YoY in Q4 2025 (driven by demand, pricing, FX, and acquisitions) and has delivered double-digit internal CAGR in the automation/robotics end-market since 2018. Adjusted EBITDA margin improved to \~19–21% recently (21.0% in Q4 2025).

Peer Comparison

Bearings-heavy peers trade in the 8–12x EV/EBITDA range (e.g., SKF, NTN analogs, or diversified industrials like RRX in power transmission). Precision/aerospace-focused names like RBC Bearings command modest premiums but still align with cyclical industrial multiples rather than secular growth. TKR’s current \~12x EV/EBITDA and \~2.1x EV/Sales reflect its diversified but mature end-markets (auto, off-highway, rail, wind) and perceived cyclicality — not the high-growth robotics optionality.

In contrast, robotics/humanoids/automation peers Timken trades at a discount. $RRX trades around 15.5x EV/EBITDA, while $MOG.A commands a much higher multiple of 21.3x EV/EBITDA. Timken sits comfortably in the middle. I believe TKR’s humanoid exposure (via the faster-growing Industrial Motion segment) is not yet fully priced in by the market.

In the Q1 2026 earnings call, CEO Lucian Boldea highlighted automation/robotics as a strategic priority where Timken has “doubled down,” delivering double-digit CAGR since 2018. Humanoids are explicitly called out as a high-potential subset addressing labor gaps: "Cone Drive and Spinea provide harmonic/cycloidal drives for joints; Rollon for 7th-axis linear; CGI for medical robotics; Timken bearings and Cone Drive harmonics already present in humanoids/exoskeletons. We are nicely positioned to benefit… We will have our newly appointed Chief Technology Officer talk more at Investor Day about the opportunity.” The company participates in humanoid summits and frames harmonic solutions as core to scaling these platforms. With Industrial Motion already outgrowing the legacy bearings segment and backlog momentum building, the humanoid/robotics tailwind represents asymmetric upside that justifies a valuation re-rating above legacy auto/aerospace multiples — toward robotics/automation peers (15–20x+ EV/EBITDA) as revenue contribution scales.

This is my thesis for $TKR not financial advise. I'm simply jotting down my notes and sharing with you all so maybe you can have a new perspective on the industry or even find critics in the thesis yo may not agree with.

u/Optimal_Image5192 — 22 days ago