1.96 Billion People. 81 Days. Southern Asia's Hormuz Crisis

May 21, 2026

This is a continuation from my previous post about South East Asia. It’s a big area so I had to split it up in to different parts. It is a long post but you can skip the rest and just read the summary. There is a link for the infographics and the key sources/Glossary. Let me know what you guys think!

https://www.reddit.com/r/oil/s/cmHObVtzLC

TLDR/Summary

February 28, 2026: Iran mines the Strait of Hormuz. Transit collapses ~90-95%. 20% of the world's oil stops moving. Southern Asia, 1.96 billion people, has no workaround.

Brent crude: $111/barrel May 19, fell to ~$106 at close May 20 as peace talks accelerated (TradingEconomics/Yahoo Finance). Middle Eastern crude trades at a premium because the disruption IS in the Gulf. The real cost to these countries is above the Brent headline.

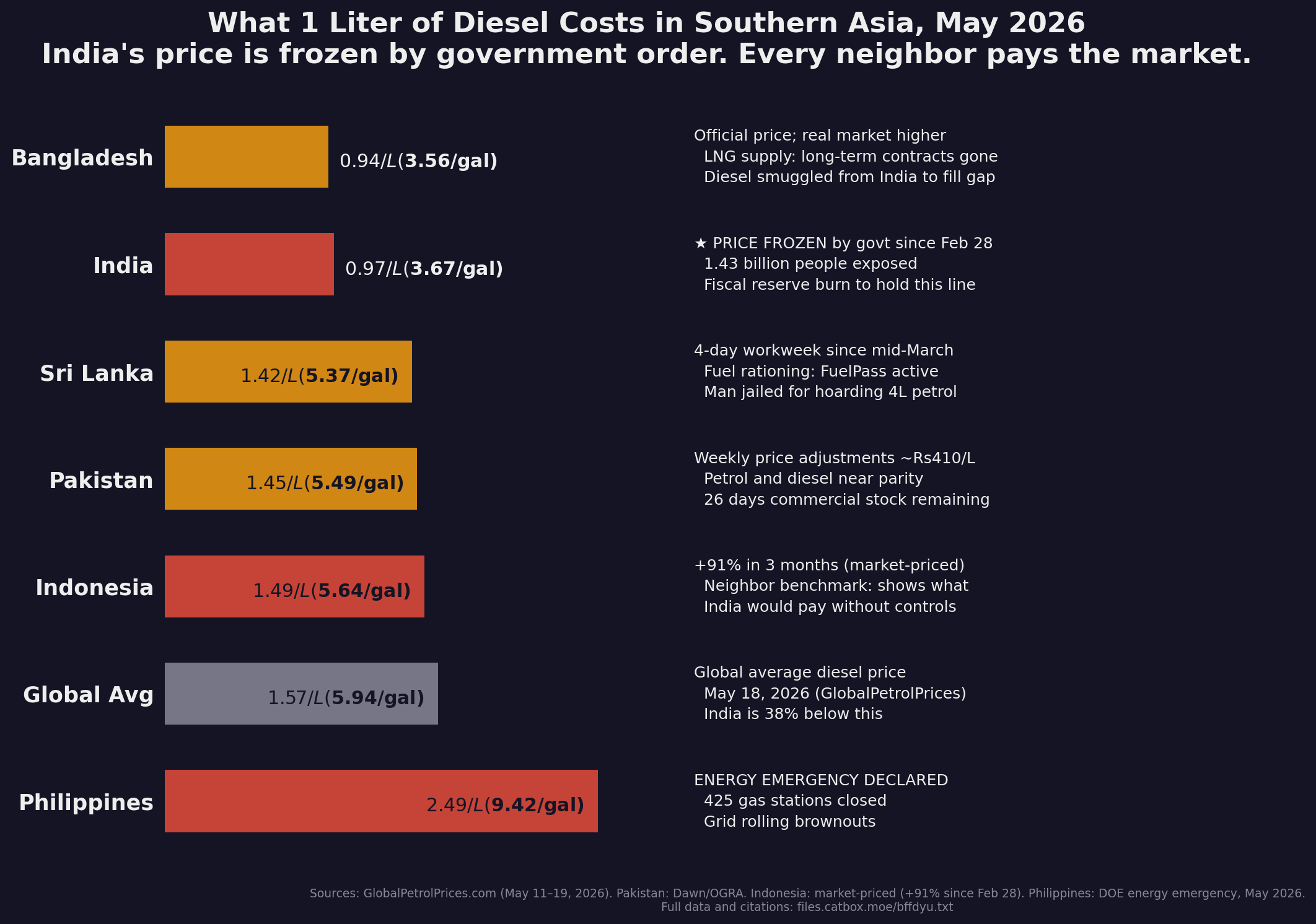

India (1.43B): Diesel frozen at $0.97/L ($3.67/gal) through excise cuts and OMC subsidies (Rs3/L hike on May 15 broke the freeze), a $0.60/L gap vs global average, costing billions a month. Forex: $697B, down $31B since February. 332M LPG connections on extended 25-45 day refill cycles. When the subsidy cracks, 1.43 billion feel it.

Pakistan (257M): ~26 days of petrol, ~25 days of diesel. Commercial working inventory, not reserves. March fuel hike of Rs55/L, largest in history. Now at Rs409.78/L petrol, Rs409.58/L diesel. Emergency diesel payments authorized (OGRA: Rs7.1B to PSO, May 13). Austerity through June 13.

Bangladesh (174M): Long-term LNG suppliers (Qatar, Shell, OQ) declared force majeure. At least 7 cargoes cancelled; forced to spot market at ~3x prices. Fertilizer plants mostly shut. Aman rice planting season approaches in July. 400+ garment factories shut in 3 years. 10-day fuel stocks, daily blackouts.

Sri Lanka (22M): 4-day workweek since mid-March. Diesel $1.42/L ($5.37/gal). $54.8B external debt, forex declining. Tourism stalling.

Nepal (31M): Landlocked, 100% dependent on India. Now Southern Asia's priciest fuel. LPG half-rationed since March 13. Remittances (~33% of GDP, roughly $14-15B) at risk if Gulf economies contract.

Afghanistan (43M): 21.9M need aid. WFP aid slashed from 10M to 2M. No oil, no reserves, no international finance. Fuel prices crippling WFP delivery.

Maldives (520K): Island nation, 100% import dependent. March tourist arrivals crashed 20.7%. Dollar black market premium ~35%. Private airline suspended until October.

A mid-March ceasefire proposal was rejected by Iran. On April 7, a two-week ceasefire was agreed to and extended. Operation Project Freedom, a US Navy escort mission launched May 4, was paused the next day. On May 18, Pakistan handed a revised Iranian peace proposal to Washington. On May 20, Trump proposed a broader peace framework to Israel, including a 30-day negotiation period and Strait of Hormuz reopening. The Strait remains effectively closed; negotiations continue for who knows how long.

If you're in Southern Asia, what are you seeing on the ground that matches or contradicts any of this?

Full glossary, sources, and infographics:

https://files.catbox.moe/08jjjf.txt

• Diesel prices comparison: https://files.catbox.moe/vw7ogd.png

• Fuel reserves comparison: https://files.catbox.moe/s7t7u1.png

{kind=link}

{kind=link}

Note: Southern Asian countries don't buy Brent. They import Middle Eastern crude priced against Dubai/Oman benchmarks, which trade at a premium during Gulf disruptions. We cite Brent because it's the global reference, the actual cost to these countries is higher.

(End of Summary)

Background

When Iranian forces mined and blockaded it on February 28, commercial shipping transit collapsed roughly 95%, traffic dropping from normal levels to near zero within days (World Economic Forum, April 2026). That removed ~17-20 million barrels per day from global markets, roughly 20% of world oil supply. The IEA calls it "the largest supply disruption since the 1970s energy crisis, and the largest in the history of the oil market." Eighty-one days later, Southern Asia still has no workaround.

A note on "closed": The Strait is not physically impassable: a few vessels still transit, paying IRGC tolls of up to $2M per ship. Even 5% of normal throughput is ~1M bpd still moving. But for the countries in this report, imports have collapsed ~90-95% and what gets through does so at ruinous cost.

What the world has done: Saudi Arabia's East-West Pipeline and the UAE's Fujairah pipeline (~6.8M bpd combined) bypass Hormuz entirely and are running near-maximum. The IEA's coordinated release of ~400M barrels from member SPRs (March 2026) bought time but is a finite bridge. After accounting for pipeline bypass and SPR releases, the remaining shortfall is roughly 10-12M bpd, what's driven the price surge (Brent peaked at $126/barrel per TradingEconomics).

Demand destruction: At $105-115 Brent, global demand doesn't sit still. IEA models suggest 1-2M bpd of demand destruction for every sustained $10 above $90. At crisis prices, 2-4M bpd is already eroding: drivers cutting trips, factories reducing shifts, airlines canceling routes. This is not a solution (it IS the crisis process for importers), but it is self-correcting. The worst-case scenarios below assume demand destruction is insufficient to close the gap.

Southern Asia has 1.96 billion people. It imports the vast majority of its oil, gas, and fertilizer through or from the Gulf. It has almost no strategic petroleum reserves. It entered this crisis already fragile: Bangladesh at 9%+ inflation, Pakistan at B- credit rating, Sri Lanka still recovering from its 2022 default. Afghanistan was already in a hunger crisis. Nepal was already rationing cylinders.

Country By Country

India: The Subsidy Trap

India imports 88-89% of its oil, roughly half normally via the Gulf and Hormuz.

Diesel: $0.97/L ($3.67/gal). Effectively frozen for nearly three months through excise duty cuts and OMC subsidies. A Rs3/L hike on May 15 broke the freeze (Reuters, May 15); the first increase since the crisis began, but retail prices remain heavily subsidized. By comparison: global average diesel is $1.57/L ($5.94/gal) (GlobalPetrolPrices, May 18). Indonesia, with market pricing, is at $1.49/L ($5.64/gal) (+91% in 3 months). India's government is absorbing the difference, roughly $15-25B in additional subsidy cost at sustained $100+ Brent. The risk is not that India runs out of money tomorrow. It's that sustained subsidies force either a sharp adjustment or a gradual squeeze, and either path hits 1.43 billion people.

LPG: The cooking fuel emergency. 332 million LPG connections. ~60% of LPG is imported, almost all through Hormuz. Middle East-origin LPG shipments fell 75-80% in March-April (Kpler). The government raised domestic production from ~36,000 tons/day to 54,000 tons/day by mid-May and secured 650,000 tons of additional supply for May. Refill turnaround, normally 5-7 days, has been extended to 25 days for urban households, 45 days for rural (Ministry of Petroleum, May 2026). Commercial LPG cylinder prices were hiked Rs993 on May 1, the largest single increase on record. Restaurants in Mumbai began shutting in March. Gujarat's ceramics industry closed entirely. Families are reverting to firewood and biomass. This is a public health crisis in slow motion.

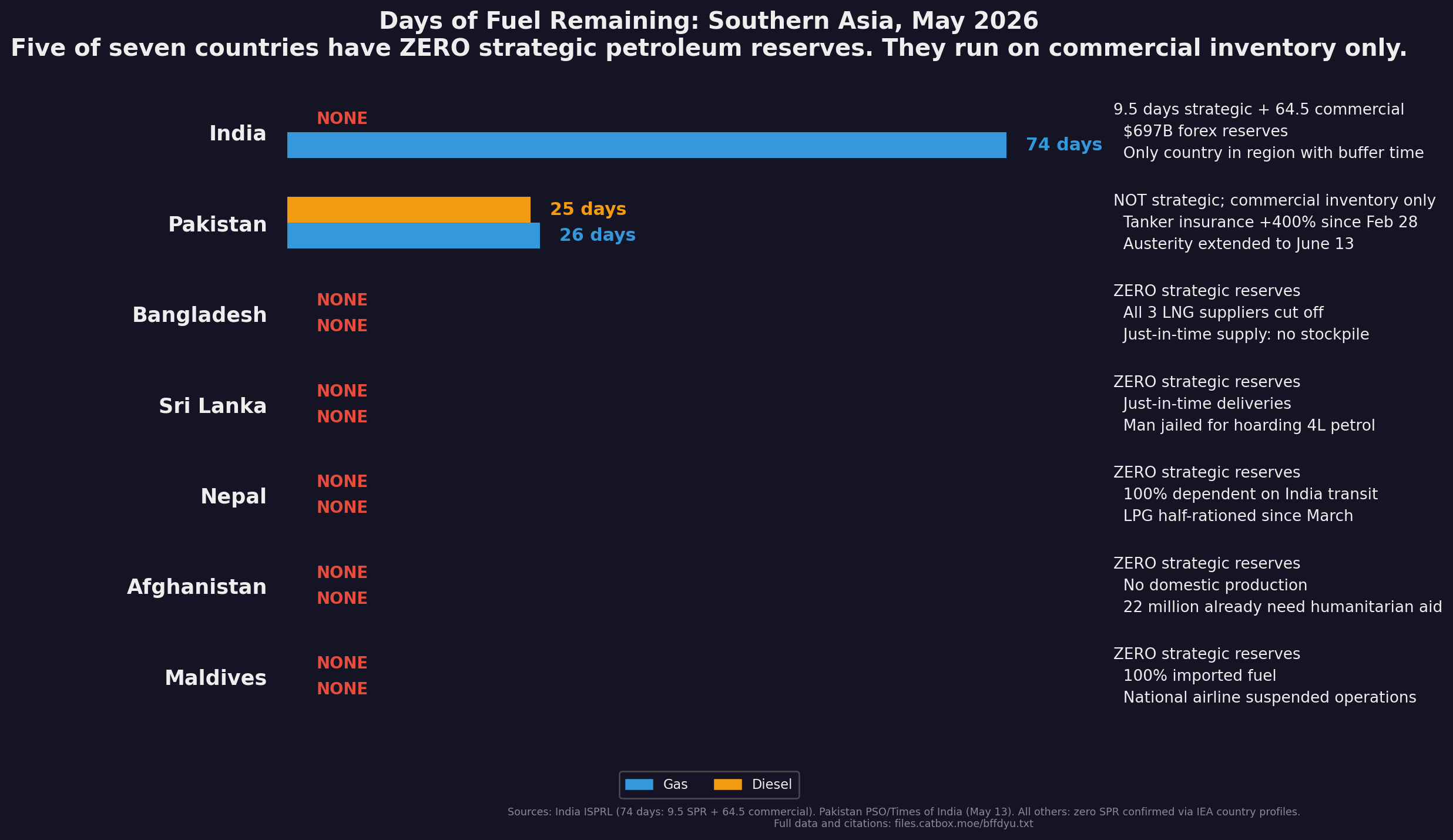

India has 74 days of total oil storage (9.5 days strategic + 64.5 days commercial). As of March, the strategic portion was only 64% full. $697B in forex reserves (RBI, May 15). ~70% coal power. India is far better positioned than its neighbors. But its 332 million LPG users have no backup. When the cylinder stops coming, the firewood starts.

Government response: Excise duties cut 10 rupees/L in late March. Export duties raised to keep supply domestic. Over 580,000 piped gas connections gasified or issued in March (domestic supply, unaffected by Hormuz). Coal power ramped up.

Pakistan: The Countdown

Pakistan spends roughly $15-17 billion annually on petroleum imports (pre-crisis run rate; weekly import bill surged from $300M to $800M, per PM Sharif, April 2026). Forex: ~$21.3B total ($15.87B SBP-held as of May 8). External debt: $138B. Credit rating: B- (S&P), Caa1 (Moody's).

Fuel stocks as of mid-May: ~26 days of petrol, ~25 days of diesel. Commercial working inventory, not strategic reserves. Pakistan has no SPR.

The math that doesn't work: At sustained $100+ oil, Pakistan's import bill approaches $30B, ~140% of total forex reserves. In March, petrol was hiked Rs55/L, the largest single increase in the country's history. By mid-May, prices sat at Rs409.78/L for petrol and Rs409.58/L for diesel after a token Rs5 cut on May 16 (Dawn). Weekly price revisions continue, but the Rs5 cut was political theater against a Rs55/L surge. OGRA ordered refineries to pay PSO Rs7.1 billion under emergency diesel pricing on May 13, confirming the crisis has reached emergency procurement levels.

Austerity: Extended through June 13. 50% cut in fuel allocations for government vehicles. 60% of government vehicles off the road. 4-day workweek. Ban on foreign travel by ministers.

The shipping crisis: Insurance exploded from near-zero to hundreds of thousands per voyage; freight from ~$900K to ~$4M per vessel. Pakistan State Oil has launched two emergency import tenders via alternative routes. Saudi Arabia has been asked to supply through the Red Sea.

Agriculture: Diesel for irrigation pumps and harvesters is at risk. Fertilizer imports through Hormuz are disrupted, threatening the kharif planting season.

Bottom line: Pakistan is not in freefall yet. Emergency tenders are securing spot cargoes at 2-3x cost. But the binding constraint is dollars: the import bill approaches ~140% of forex reserves at sustained crisis prices. Draw down the ~26-day working inventory without replacement and the system seizes. If alternative supply doesn't deliver by early June, escalating rationing is inevitable.

Bangladesh: The Silent Collapse

Bangladesh imports most of its oil and all of its LNG. Its energy mix: natural gas ~46-50% (down from 68%), oil ~22%, coal ~12-28%. It was scheduled for 115 LNG cargoes in 2026. After Qatar, its largest supplier, declared force majeure on March 3, other contracted suppliers (Shell, OQ) followed within days. At least 7 cargoes were cancelled. Bangladesh was forced to the spot market at nearly 3x pre-crisis prices. Spot LNG at $25-30/mmBtu prices its forex position cannot sustain at scale. The gas is physically available; the dollars to buy it are not. Forex: $35.1B gross, $30.5B net (April 24). External debt: $112B. Inflation: 9.04% (April 2026).

Fertilizer: The majority of Bangladesh's fertilizer plants are shut, lacking gas feedstock. Agriculture employs 35% of the workforce. Rice is the staple. The aman rice planting season (July-December) is approaching. Without fertilizer, yields drop substantially.

Garment industry: $38.8 billion in exports, the backbone of the economy. Over 400 garment factories have shut in three years even before the crisis, and the survivors need diesel for backup power and gas for production. Both are scarce. Industry groups are begging for emergency diesel allocations. International buyers will shift orders to countries with stable energy if disruptions continue: once supply chains reroute, they don't come back.

Government response: Universities closed early for Eid. Malls ordered closed by 7 PM. Coal power ramped up, but capacity is limited. Loadshedding daily; rural areas, where poverty is deepest, get the longest cuts.

Fuel prices: Diesel Tk 115/L ($0.94/L, $3.56/gal), petrol Tk 135/L ($1.10/L, $4.16/gal), octane Tk 140/L ($1.14/L, $4.32/gal). On April 19, Bangladesh raised all to record highs (diesel +Tk 15, octane +Tk 20, petrol +Tk 19), surpassing the 2022 Ukraine war peak. Prices are set by the Bangladesh Petroleum Corporation, not the market, so they appear administratively low. The crisis manifests as supply shortages: 10-day diesel stocks, queues at pumps.

Bottom line: No gas means no fertilizer. No fertilizer means lower yields. Lower yields mean higher food prices. Higher food prices mean garment workers cannot afford rice. This is the cascade that turns an energy crisis into a food crisis.

Sri Lanka: The Fragile Recovery, Crushed

Sri Lanka defaulted on its sovereign debt in 2022. It spent two years in an IMF program, clawing back to 5% GDP growth in 2024 and 2025. The Hormuz crisis has undone that recovery.

The 4-day workweek began in mid-March. Wednesdays off for public institutions. In effect until fuel supply improves. Indefinite.

The severity signal: In March 2026, a 48-year-old man was sentenced to three weeks in prison for hoarding 4 liters of petrol. An emergency spot cargo during the peak of the March panic reportedly cost $286 per barrel, confirmed by HSBC's CEO in April as "as high as $286 in at least one case" (Middle East Eye, April 15). A single cargo at the most extreme moment, not Sri Lanka's ongoing import cost. Ceylon Petroleum Corporation says its contracted crude is $72-113/barrel. Even at the lower end, the shipping premiums are punishing.

Fuel rationing: FuelPass quota system active. Weekly limits by vehicle type (~15L for cars), Sunday resets, odd-even in some areas. Current prices: diesel $1.42/L ($5.37/gal), 95 Octane $1.46/L ($5.53/gal). These are government-managed and don't guarantee fuel is actually at the pump.

Forex: $7.2B (February, declining to $7.0B by March). External debt: $54.8B. Government debt: $96.9B (91.6% of GDP). Cannot afford another round of crisis spending. No strategic reserves. Just-in-time commercial inventory. Any disruption causes immediate shortages. Being an island compounds it with a shipping premium on everything.

Tourism: The recovery engine is stalling. Airlines canceling routes. European and Middle Eastern tourists staying home. The Gulf, normally a source of visitors and remittances, is a war zone.

Bottom line: Sri Lanka was just getting back on its feet. The 2022 default recovery took two years. Now reserves are declining, tourism is collapsing, and there is no fuel buffer. The risk of slipping back toward crisis territory is real.

Nepal: The Transit Trap

Population: 31 million. GDP per capita: ~$1,500.

Nepal is landlocked between India and China. Every liter of oil and LPG enters through India. India's subsidized fuel system is Nepal's supply chain. India's LPG crisis is Nepal's LPG crisis. As of May 2026, Nepal is Southern Asia's priciest place to fill a tank (Global Voices, May 7).

LPG rationing began March 13. The state-run Nepal Oil Corporation now refills only half of each consumer's empty cylinder, citing the need to "lengthen liquid petroleum stockpiles" (Reuters, March 12). Half-cylinder rationing means families consume less. Triage, not stability. LPG is the primary cooking fuel for urban Nepal. Rural households rely on firewood and biomass: deforestation and respiratory illness. The half-cylinder policy hits urban families hardest, exactly the population with no fallback.

Remittances: Roughly 33% of GDP (~$14-15B annually), from Nepali workers in the Gulf, Malaysia, and South Korea. Remittances grew 31.9% in dollar terms through Q3 FY2025-26 (Kathmandu Post). But that was before the Hormuz crisis fully hit. If Gulf economies contract, the pipeline funding a third of Nepal's GDP shrinks. For families depending on a relative abroad for food and fuel money, the crisis hits twice: the fuel costs more, and the money to buy it may disappear.

Tourism: Everest spring and autumn trekking are Nepal's two forex windows. Fuel costs drive airfares higher. The autumn season faces real headwinds.

Bottom line: Nepal's crisis is downstream of India's. If India's subsidy regime cracks, Nepal feels it first: the supply chain reaches Nepal last. The half-cylinder rationing is the warning shot.

Afghanistan: The Hunger Crisis That Fuel Prices Will Break

Population: 43 million. GDP per capita: ~$360.

Afghanistan was already in one of the world's worst humanitarian crises: 21.9 million people (nearly half the population) require humanitarian assistance. Nearly 5 million mothers and children are affected by malnutrition. WFP cut food assistance from 10 million people to just 2 million earlier this year due to a funding crisis, and warned on May 15, 2026 that soaring fuel prices and disrupted Middle East supply routes are pushing operational costs higher (UN News).

The Taliban government has no access to international finance, no strategic reserves, no oil production, no refining capacity. Afghanistan imports all fuel, primarily through Pakistan and Iran, both in crisis.

Over 600,000 Afghans have returned from Iran and Pakistan in the first four months of 2026, arriving in a country with no jobs, no fuel, and no food surplus. Food prices have eased slightly from their peak but remain unaffordable for most (WFP). When diesel doubles, food transport doubles. In a country where 90%+ of the population is food-insecure, the margin between hunger and famine disappears.

The Hormuz crisis is not the cause of Afghanistan's hunger. It is the multiplier. When aid agencies cannot afford fuel for trucks, food does not move.

Maldives: The Luxury Destination Running on Empty

Population: 520,000. 1,192 islands. Imports everything. Tourism generates the dollars to pay for it: $361M in tourism tax revenue in 2025.

The dollar crisis predates Hormuz. The black market USD rate was MVR 19.70 in mid-2025 (28% premium over official MVR 15.42). By May 2026 the premium widened to ~35%. Importers couldn't get dollars from banks before the crisis. Now they can't get fuel at any price.

Beond, a private all-business-class airline, suspended all flights until October 2026 citing fuel prices and Middle East airspace closures. Tourist arrivals crashed 20.7% in March alone; annual projection is 4-6% decline with revenue losses exceeding $500 million.

Richest country in Southern Asia per capita, but the most brittle. Every link: jets, generators, speedboats, cargo ships, runs on petroleum. When any link breaks, the Maldives becomes unreachable.

Bhutan (790K)

Landlocked in the Himalayas, 100% dependent on India for fuel transit. India's managed fuel pricing and supply determine Bhutan's fuel access. The economy is small enough that India can absorb the cost for now. If India's own supply tightens, Bhutan is at the end of the pipe.

Why Southern Asia Breaks First

- LPG is survival, not convenience. Hundreds of millions cook every meal with it. No scalable alternative. Piped gas is rare. Electric cooking requires a grid already strained. The fallback is firewood and biomass: respiratory disease, deforestation, hours of labor borne by women.

- The landlocked amplify the coastal crisis. Nepal, Afghanistan, and Bhutan have no ports. Every barrel crosses a border from a neighbor also in crisis. The transit countries get supply first. The landlocked get what's left. India and Pakistan are ramping coal generation, but coal imports face the same shipping chaos: triage, not strategy.

Scenarios

Best case: Strait reopens by July following a diplomatic resolution. The May 20 Trump peace framework and the May 18 Pakistani-mediated Iranian proposal are the two active tracks. Demand destruction (~2-4M bpd) combines with resumed Gulf supply to push oil toward $80-90. The IEA's 400M-barrel emergency release bridged the gap. Pakistan stretches its buffer through alternative supply. India eases LPG controls gradually. Bangladesh restarts fertilizer plants for late aman planting. Nepal's rationing ends. Sri Lanka avoids default. Recovery begins late Q3.

Base case (what the data supports): Strait remains disrupted through summer. Brent $95-125. Demand destruction accelerates but cannot fully close a 10-12M bpd supply gap. Pakistan exhausts commercial stocks by mid-June, shifts to emergency allocation. The constraint is dollars, not physical supply, but the result is escalating rationing. India holds diesel subsidies through June but begins a gradual adjustment. Bangladesh loses the aman planting season, rice yields down 20-30%. Sri Lanka's forex runs out, default by August. Nepal's rationing deepens as India diverts supply inward. Afghanistan's aid delivery system breaks down. Maldives tourism collapses.

Worst case: Strait closed through 2026, no diplomatic resolution. Brent $150+. Demand destruction hits 5-7M bpd, a deep recession. Pakistan: fuel for military and hospitals only; agriculture collapses. Bangladesh: severe food crisis as aman and boro rice cycles disrupted, garment industry loses half its orders. India: tens of millions revert to biomass cooking as LPG refill periods extend past survivable limits. Nepal: cylinders stop, urban crisis turns rural. Afghanistan: mass starvation. Maldives: ceases to function as an economy. Sri Lanka: hospitals without power, water treatment without chemicals.

What Can Be Done

Governments: Ration by priority sector BEFORE reserves hit tank bottoms: food first, hospitals second. Secure LPG from alternative sources at any diplomatic cost. Cash transfers to the poor, not fuel subsidies that subsidize SUV owners. Prioritize diesel for irrigation pumps and food transport. Build strategic reserves to 90 days minimum. Tell people what's coming: silence breeds panic.

Fuel prices, reserve levels, and crisis conditions change rapidly. All claims cited with links where available. Scenario projections are analysis, not predictions.

{kind=link}

{kind=link}